Access Investments-Building Awareness - European Union-ROMANIA

Showing posts with label Uniunea europeana. Show all posts

Showing posts with label Uniunea europeana. Show all posts

Friday, December 23, 2016

Monday, December 19, 2016

At least nine people have been killed and many more injured, according to German police, after a truck ploughed into a Christmas market in Berlin in what is believed to have been a deliberate attack. A vehicle, a large black Scania articulated lorry, ran into the market outside the landmark Kaiser Wilhelm memorial church on Monday evening. German police said one person was found dead in the lorry, having died of injuries sustained in the crash, while a suspect was arrested about 100 metres away from the scene in the Tiergarten. A witness told the Guardian that the truck ploughed into the market at speed. “It was not an accident. The truck was going 40mph. It was in the middle of a square, there are main roads either side, [where it could have come from]. But it showed no sign of slowing down,” said Emma Rushton. She said it crashed into a stall only a few feet from where she and her friend were standing. “We heard a massive bang. About eight to 10 feet in front of us was where the lorry ploughed through. It ploughed through the stall where we bought our mulled wine.

“It ploughed through people and the wooden huts, it tore the lights down. Everything went dark, it was black and there was screaming. It was awful,” she said.

Wednesday, December 14, 2016

Reuters writes that the 2 billion Euros "investment" needs to be approved by the European Commission, which needs to check whether the transaction occurs at the market price or if it represents a state aid. Shortly after, a report appeared in Italian daily La Stampa, where it is state that the authorities in Rome have asked for a 15 billion Euros financial aid from the European Stability Mechanism (ESM) to prop up Italy's banking system. Shares of Italian banks rose significantly following the news, with Monte dei Paschi, being the best "performer", with a rise of about 10%. "No request for the ESM is being prepared", a spokesperson of the Italian treasury said, according to Financial Times. With the resignation of the government led by Matteo Renzi, who has announced on his Twitter account that the budget law has been approved, Italy's "Aeneid" in the Eurozone enters a new stage and nobody knows when the country is going to turn that corner. As for Greece's "Odyssey", Bloomberg asks whether the plan to cut the debt burden isn't too small and applied too late, reminding that the IMF sees the fiscal targets as unrealistic and the debt as far too big. Right now all we have to do is wait, even though we probably won't have to wait as many years as have passed since the aggravated phase of the sovereign debt in Europe, to find out whether Greece and Italy will "kick the bucket" once they "turn that corner".

Reuters writes that the 2 billion Euros "investment" needs to be approved by the European Commission, which needs to check whether the transaction occurs at the market price or if it represents a state aid. Shortly after, a report appeared in Italian daily La Stampa, where it is state that the authorities in Rome have asked for a 15 billion Euros financial aid from the European Stability Mechanism (ESM) to prop up Italy's banking system. Shares of Italian banks rose significantly following the news, with Monte dei Paschi, being the best "performer", with a rise of about 10%. "No request for the ESM is being prepared", a spokesperson of the Italian treasury said, according to Financial Times. With the resignation of the government led by Matteo Renzi, who has announced on his Twitter account that the budget law has been approved, Italy's "Aeneid" in the Eurozone enters a new stage and nobody knows when the country is going to turn that corner. As for Greece's "Odyssey", Bloomberg asks whether the plan to cut the debt burden isn't too small and applied too late, reminding that the IMF sees the fiscal targets as unrealistic and the debt as far too big. Right now all we have to do is wait, even though we probably won't have to wait as many years as have passed since the aggravated phase of the sovereign debt in Europe, to find out whether Greece and Italy will "kick the bucket" once they "turn that corner". Tuesday, September 20, 2016

Once upon a time, there were five international audit, tax and audit consulting firms. Arthur Andersen disappeared in 2002, after it was convicted for the involvement in the Enron fraud. Since then, there have been four giants on this market, PricewaterhouseCoopers (PwC), Deloitte Touche Tohmatsu, Ernst & Young and KPMG, and some of their biggest clients are financial institutions. Bloomberg and Financial Times recently wrote that PricewaterhouseCoopers has been sued for "not having detected a case of fraud that led to the collapse of a bank during the global financial crisis". According to FT, the lawsuit in the United States "could bring more audit firms in the line of fire". The biggest lawsuit against an audit firm, according to Financial Times, has been brought following the complaint filed by the company that is in charge of the liquidation of Taylor, Bean & Whitaker (TBW), a mortgage originator in the US, which has been in a long-lasting relationship with Colonial Bank din Alabama. During the period of the real estate bubble in the United States, which has led to the subprime lending crisis, TBW used to grant mortgage loans, and they have already been financed by Colonial Bank. According to the article in FT, the company that manages what is left of the TBW assets are accusing PwC of "failing to spot the conspiracy of several billion dollars between the founder of TBW and the executive management of Colonial Bank". The documents submitted to the court show that PwC signed "clean" audit opinions between 2002 and 2008, and in 2009 Colonial Bank collapsed and "rose" up to the 6th position in the chart of the biggest defaults in the US. The cost for the FDIC (author's note": Federal Deposit Insurance Corp., the institution for the guarantee of bank deposits in the US) was 4.2 billion dollars, according to Bloomberg estimates.

Once upon a time, there were five international audit, tax and audit consulting firms. Arthur Andersen disappeared in 2002, after it was convicted for the involvement in the Enron fraud. Since then, there have been four giants on this market, PricewaterhouseCoopers (PwC), Deloitte Touche Tohmatsu, Ernst & Young and KPMG, and some of their biggest clients are financial institutions. Bloomberg and Financial Times recently wrote that PricewaterhouseCoopers has been sued for "not having detected a case of fraud that led to the collapse of a bank during the global financial crisis". According to FT, the lawsuit in the United States "could bring more audit firms in the line of fire". The biggest lawsuit against an audit firm, according to Financial Times, has been brought following the complaint filed by the company that is in charge of the liquidation of Taylor, Bean & Whitaker (TBW), a mortgage originator in the US, which has been in a long-lasting relationship with Colonial Bank din Alabama. During the period of the real estate bubble in the United States, which has led to the subprime lending crisis, TBW used to grant mortgage loans, and they have already been financed by Colonial Bank. According to the article in FT, the company that manages what is left of the TBW assets are accusing PwC of "failing to spot the conspiracy of several billion dollars between the founder of TBW and the executive management of Colonial Bank". The documents submitted to the court show that PwC signed "clean" audit opinions between 2002 and 2008, and in 2009 Colonial Bank collapsed and "rose" up to the 6th position in the chart of the biggest defaults in the US. The cost for the FDIC (author's note": Federal Deposit Insurance Corp., the institution for the guarantee of bank deposits in the US) was 4.2 billion dollars, according to Bloomberg estimates.Saturday, September 17, 2016

EU leaders will search for unity at a special summit without the UK on Friday, in the hope of setting a course for a union battered by the Brexit vote and riven by a simmering east-west row over migration. Donald Tusk, the former Polish prime minister who chairs EU leaders’ summits, hopes to cool tempers after Luxembourg’s foreign minister called for Hungary to be thrown out of the EU for allegedly treating asylum seekers “worse than wild animals”. Hungary counterattacked with stinging criticism of the grand duchy’s record in helping big corporations avoid tax. On Thursday Tusk called on EU leaders to take a “brutally honest” look at the bloc’s problems, declaring: “We must not let this crisis go to waste.” “We haven’t come to Bratislava to comfort each other or even worse to deny the real challenges we face in this particular moment in the history of our community after the vote in the UK,” said Tusk, who will chair the summit. “We can’t start our discussion ... with this kind of blissful conviction that nothing is wrong, that everything was and is OK,” he added. “We have to assure ... our citizens that we have learned the lesson from Brexit and we are able to bring back stability and a sense of security and effective protection.” Tusk hopes to focus on areas that the 27 leaders can agree on: border security, counter-terrorism and moves to “to bring back control of globalisation”. Officials are playing down expectations of results from the meeting at Bratislava castle, in the capital of Slovakia, one of the four Visegrád countries along with Poland, Hungary and the Czech Republic. Officials close to Tusk hope for small but symbolic breakthroughs, most notably an agreement to send an extra 200 border guards and 50 vehicles to the EU’s external frontier in Bulgaria by next month. Agreeing on stronger border defences is the easy bit. The thorny issue of sharing the cost of protecting refugees is likely to continue to strain unity. The Visegrád group are fiercely opposed to the EU executive’s attempts to fine them for not accepting refugees in their countries. Hungary has flatly refused to take in refugees under an EU quota scheme, while many other countries are falling short. Hungary’s rightwing prime minister, Viktor Orbán, has called a referendum for 2 October on the EU relocation plan, which would see 1,294 asylum seekers sent to the country. Ahead of the vote, the European commission president, Jean-Claude Juncker, appeared to offer an olive branch to his opponents. In his annual state of the union address, he said solidarity “must come from the heart” and could not be forced.

Wednesday, September 14, 2016

An authoritarian European Commission was to blame for Brexit and must give up on its federalist dreams or risk the disintegration of the European Union, eastern European states have warned as the continent’s divisions were laid bare. “The EU has to change, we have to reform it," the Polish Prime Minister Beata Szydlo told the European Council president, Donald Tusk, at a meeting in Warsaw designed to ensure that post-Brexit Europe could present a united front at a summit in Bratislava on Friday. The east-west split in Warsaw came on the eve of today’s keynote ‘State of the Union’ speech by Jean-Claude Juncker, the European Commission president, which aides had also hoped would provide a “big bang” moment to show that Europe could deliver for ordinary citizens. Instead, European capitals descended into a round of bitter mutual recrimination over the future direction of the continent.

An authoritarian European Commission was to blame for Brexit and must give up on its federalist dreams or risk the disintegration of the European Union, eastern European states have warned as the continent’s divisions were laid bare. “The EU has to change, we have to reform it," the Polish Prime Minister Beata Szydlo told the European Council president, Donald Tusk, at a meeting in Warsaw designed to ensure that post-Brexit Europe could present a united front at a summit in Bratislava on Friday. The east-west split in Warsaw came on the eve of today’s keynote ‘State of the Union’ speech by Jean-Claude Juncker, the European Commission president, which aides had also hoped would provide a “big bang” moment to show that Europe could deliver for ordinary citizens. Instead, European capitals descended into a round of bitter mutual recrimination over the future direction of the continent.Monday, September 12, 2016

France’s opposition party will field eight candidates in primaries to decide who will lead it in next year’s presidential election. Polls suggest the winner of the November two-round party vote will become the country’s next leader.

France’s opposition party will field eight candidates in primaries to decide who will lead it in next year’s presidential election. Polls suggest the winner of the November two-round party vote will become the country’s next leader.

After Les Républicains (LR) party nominations closed on Friday evening, the stage was set for a rightwing “duel” between former president Nicolas Sarkozy and former prime minister Alain Juppé, now mayor of Bordeaux.

Polls predict that whoever wins the primary will be in the second-round runoff next May against the Front National’s Marine Le Pen; the latest show Juppé, 71, still the favourite with LR voters, but Sarkozy, 61, snapping at his heels. According to market researchers TNS Sofres, if the election were held tomorrow Juppé would win the second round against Le Pen with 55% of votes, but pollsters agree that former Socialist finance minister Emmanuel Macron could seriously upset the contest if he decides to stand. Macron, an ex-banker, resigned from the Socialist government last month but has not said if he will join the presidential race. Le Figaro suggests he would knock out Sarkozy to take third place.

The only woman among the eight LR candidates, former minister Nathalie Kosciusko-Morizet, 43, is an outside bet.

Saturday, September 10, 2016

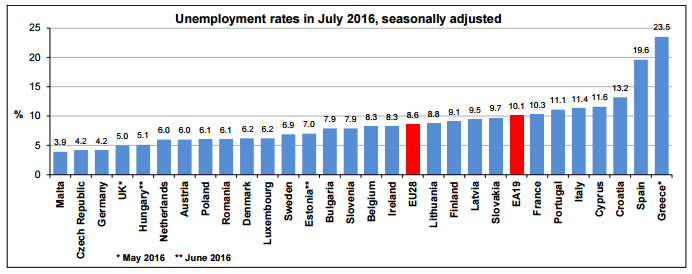

Eurostat has issued a publication to inform regarding the unemployment rate in Euro area for July.The euro area (EA19) seasonally-adjusted unemployment rate was 10.1% in July 2016, stable compared to June 2016 and down from 10.8% in July 2015. This remains the lowest rate recorded in the euro area since July 2011. The EU28 unemployment rate was 8.6% in July 2016, stable compared to June 2016 and down from 9.4% in July 2015. This remains the lowest rate recorded in the EU28 since March 2009. These figures are published by Eurostat, the statistical office of the European Union. Eurostat estimates that 21.063 million men and women in the EU28, of whom 16.307 million were in the euro area, were unemployed in July 2016. Compared with June 2016, the number of persons unemployed decreased by 29 000 in the EU28 and by 43 000 in the euro area. Compared with July 2015, unemployment fell by 1.688 million in the EU28 and by 1.034 million in the euro area.

Eurostat has issued a publication to inform regarding the unemployment rate in Euro area for July.The euro area (EA19) seasonally-adjusted unemployment rate was 10.1% in July 2016, stable compared to June 2016 and down from 10.8% in July 2015. This remains the lowest rate recorded in the euro area since July 2011. The EU28 unemployment rate was 8.6% in July 2016, stable compared to June 2016 and down from 9.4% in July 2015. This remains the lowest rate recorded in the EU28 since March 2009. These figures are published by Eurostat, the statistical office of the European Union. Eurostat estimates that 21.063 million men and women in the EU28, of whom 16.307 million were in the euro area, were unemployed in July 2016. Compared with June 2016, the number of persons unemployed decreased by 29 000 in the EU28 and by 43 000 in the euro area. Compared with July 2015, unemployment fell by 1.688 million in the EU28 and by 1.034 million in the euro area.

Member States

Among the Member States, the lowest unemployment rates in July 2016 were recorded in Malta (3.9%) as well as in the Czech Republic and Germany (both 4.2%). The highest unemployment rates were observed in Greece (23.5% in May 2016) and Spain (19.6%). Compared with a year ago, the unemployment rate in July 2016 fell in twenty-four Member States, remained stable in Denmark, while it increased in Estonia (from 6.1% to 7.0% between June 2015 and June 2016), Austria (from 5.7% to 6.0%) and Belgium (from 8.1% to 8.3%). The largest decreases were registered in Cyprus (from 15.0% to 11.6%), Croatia (from 16.5% to 13.2%) and Spain (from 21.9% to 19.6%). In July 2016, the unemployment rate in the United States was 4.9%, stable compared to June 2016 and down from 5.3% in July 2015.

Youth unemployment

In July 2016, 4.276 million young persons (under 25) were unemployed in the EU28, of whom 2.969 million were in the euro area. Compared with July 2015, youth unemployment decreased by 310 000 in the EU28 and by 136 000 in the euro area. In July 2016, the youth unemployment rate was 18.8% in the EU28 and 21.1% in the euro area, compared with 20.2% and 22.1% respectively in July 2015. In July 2016, the lowest rates were observed in Malta (7.1%) and Germany (7.2%), and the highest in Greece (50.3% in May 2016), Spain (43.9%) and Italy (39.2%).

Geographical information

The euro area (EA19) includes Belgium, Germany, Estonia, Ireland, Greece, Spain, France, Italy, Cyprus, Latvia, Lithuania, Luxembourg, Malta, the Netherlands, Austria, Portugal, Slovenia, Slovakia and Finland. The European Union (EU28) includes Belgium, Bulgaria, the Czech Republic, Denmark, Germany, Estonia, Ireland, Greece, Spain, France, Croatia, Italy, Cyprus, Latvia, Lithuania, Luxembourg, Hungary, Malta, the Netherlands, Austria, Poland, Portugal, Romania, Slovenia, Slovakia, Finland, Sweden and the United Kingdom.

Methods and definition

Eurostat produces harmonised unemployment rates for individual EU Member States, the euro area and the EU. These unemployment rates are based on the definition recommended by the International Labour Organisation (ILO). The measurement is based on a harmonised source, the European Union Labour Force Survey (LFS).

Based on the ILO definition, Eurostat defines unemployed persons as persons aged 15 to 74 who:

- are without work;

- are available to start work within the next two weeks;

- and have actively sought employment at some time during the previous four weeks.

- are without work;

- are available to start work within the next two weeks;

- and have actively sought employment at some time during the previous four weeks.

The unemployment rate is the number of people unemployed as a percentage of the labour force. The labour force is the total number of people employed plus unemployed. In this news release unemployment rates are based on employment and unemployment data covering persons aged 15 to 74. The youth unemployment rate is the number of people aged 15 to 24 unemployed as a percentage of the labour force of the same age. Therefore, the youth unemployment rate should not be interpreted as the share of jobless people in the overall youth population.

Country notes

Germany, the Netherlands, Austria, Finland, Sweden and Iceland: the trend component is used instead of the more volatile seasonally adjusted data. Denmark, Estonia, Hungary, Portugal, the United Kingdom and Norway: 3-month moving averages of LFS data are used instead of pure monthly indicators.

Thursday, September 8, 2016

French president, Francois Hollande, will inaugurate the Airbus plant in Ghimbav on September 13th, according to sources close to the investors. According to Serge Durand, the CEO of Airbus Helicopters Industries, the first helicopter made in Ghimbav will only be delivered at the end of 2017, but starting with September 2016, the plant will become functional and operational. The company intends to bring in other projects to Braşov if the H215 project proves to be successful. Serge Durand said: "For now, we have concluded a protocol with Romanian airlines- IAR Ghimbav, Aerostar, Aerotech and Turbomecanica - to become suppliers for the helicopter that will be manufactured in Romania, which will be entirely made out of parts manufactured in Romania". Serge Durand also stated that Ghimbav will first of all manufacture the civilian version of H215, with production of the military version to be transferred in a few years from the factory in France to the one in Braşov. Moreover, in 2019, Durand hopes that over 30 Romanian engineers will be working on the design of the helicopters that will be manufactured in Ghimbav, with the company intending to develop an R&D center in Romania. The amount of the total investment in the new Airbus Helicopters project in Ghimbav is 55.7 million Euros, of which the aid of the Romanian state is a maximum of 5.2 million Euros. "We will reach 350 employees at the plant of in 2019, when we are going to start manufacturing 15 H215 helicopters a year", Durand further said. Guillaume Faury, CEO Airbus Helicopters, said that in Ghimbav will be assembled the H215 helicopter, the latest member of the H aircraft family of the German French group, the "smaller" brother of H225. H215 is an advanced variant of the former AS332 Cie/L1e helicopter, which would be sold at "accessible prices", because "the costs are low". Airbus Helicopters, a division of Airbus Group, offers solutions for civilian and military helicopters all over the world. The company has an operational fleet of approximately 12,000 helicopters operated by over 3,000 customers in approximately 154 countries. Airbus Helicopters has over 22,000 employees all over the world and has generated a revenue of 6.8 billion Euros in 2015.

French president, Francois Hollande, will inaugurate the Airbus plant in Ghimbav on September 13th, according to sources close to the investors. According to Serge Durand, the CEO of Airbus Helicopters Industries, the first helicopter made in Ghimbav will only be delivered at the end of 2017, but starting with September 2016, the plant will become functional and operational. The company intends to bring in other projects to Braşov if the H215 project proves to be successful. Serge Durand said: "For now, we have concluded a protocol with Romanian airlines- IAR Ghimbav, Aerostar, Aerotech and Turbomecanica - to become suppliers for the helicopter that will be manufactured in Romania, which will be entirely made out of parts manufactured in Romania". Serge Durand also stated that Ghimbav will first of all manufacture the civilian version of H215, with production of the military version to be transferred in a few years from the factory in France to the one in Braşov. Moreover, in 2019, Durand hopes that over 30 Romanian engineers will be working on the design of the helicopters that will be manufactured in Ghimbav, with the company intending to develop an R&D center in Romania. The amount of the total investment in the new Airbus Helicopters project in Ghimbav is 55.7 million Euros, of which the aid of the Romanian state is a maximum of 5.2 million Euros. "We will reach 350 employees at the plant of in 2019, when we are going to start manufacturing 15 H215 helicopters a year", Durand further said. Guillaume Faury, CEO Airbus Helicopters, said that in Ghimbav will be assembled the H215 helicopter, the latest member of the H aircraft family of the German French group, the "smaller" brother of H225. H215 is an advanced variant of the former AS332 Cie/L1e helicopter, which would be sold at "accessible prices", because "the costs are low". Airbus Helicopters, a division of Airbus Group, offers solutions for civilian and military helicopters all over the world. The company has an operational fleet of approximately 12,000 helicopters operated by over 3,000 customers in approximately 154 countries. Airbus Helicopters has over 22,000 employees all over the world and has generated a revenue of 6.8 billion Euros in 2015. Wednesday, September 7, 2016

The annual inflation rate in the Eurozone has remained stable in August compared to July, at 0.2%, according to a preliminary estimate published on Wednesday by the European Statistics Office (Eurostat). According to Eurostat, in the month of August, the most significant price increases were seem in food, alcohol and cigarettes, which have posted an annual increase of 1.3%, compared to 1.4% in July, followed by services, which have seen an annual increase of 1.1%, compared to 1.2% seen in July. On the other hand, energy prices have seen an annual decrease of 5.7% in August, compared to a decline of 6.7% seen in July. Eurostat had previously announced that in July, compared to June 2016, annual inflation dropped in nine EU member countries, has remained stable in seven countries and has increased in 12 states, including Romania, according to Agerpres. Eurostat has also announced on Wednesday that in July 2016, compared to June 2016, the unemployment rate has remained stable at 10.1% in the Eurozone, while in the European Union the unemployment rate has remained stable at 8.6%. Among the member states, the highest unemployment rates were seen in Greece, (23.5% in May 2016) and Spain (19.6%). On the opposite is Malta, with an unemployment rate of 3.9%, Czech Republic and Germany, both with 4.2%. Romania is below the EU average, with an unemployment rate of 6.1%. Compared to the situation in July 2015, the unemployment rate decreased in 24 member states, including Romania, has remained stable in Denmark and has increased in Estonia, Austria and Belgium. In Romania's case, according to data notified by the National Statistics Institute, (INS), the annual inflation has remained in negative territory in July as well, at -0.8%, down from -0.7% in June. Calculated based on the harmonized consumer price index, the drop has been -0.3%, the INS states. The seasonally adjusted unemployment rate also stood at 6.1%, at the end of July, up 0.1 percentage points over the previous month (6%), according to the standards of the International Labor Bureau.

Tuesday, September 6, 2016

Monday, September 5, 2016

The annual inflation rate in the Eurozone has remained stable in August compared to July, at 0.2%, according to a preliminary estimate published on Wednesday by the European Statistics Office (Eurostat). According to Eurostat, in the month of August, the most significant price increases were seem in food, alcohol and cigarettes, which have posted an annual increase of 1.3%, compared to 1.4% in July, followed by services, which have seen an annual increase of 1.1%, compared to 1.2% seen in July. On the other hand, energy prices have seen an annual decrease of 5.7% in August, compared to a decline of 6.7% seen in July. Eurostat had previously announced that in July, compared to June 2016, annual inflation dropped in nine EU member countries, has remained stable in seven countries and has increased in 12 states, including Romania, according to Agerpres. Eurostat has also announced on Wednesday that in July 2016, compared to June 2016, the unemployment rate has remained stable at 10.1% in the Eurozone, while in the European Union the unemployment rate has remained stable at 8.6%. Among the member states, the highest unemployment rates were seen in Greece, (23.5% in May 2016) and Spain (19.6%). On the opposite is Malta, with an unemployment rate of 3.9%, Czech Republic and Germany, both with 4.2%. Romania is below the EU average, with an unemployment rate of 6.1%. Compared to the situation in July 2015, the unemployment rate decreased in 24 member states, including Romania, has remained stable in Denmark and has increased in Estonia, Austria and Belgium. In Romania's case, according to data notified by the National Statistics Institute, (INS), the annual inflation has remained in negative territory in July as well, at -0.8%, down from -0.7% in June. Calculated based on the harmonized consumer price index, the drop has been -0.3%, the INS states. The seasonally adjusted unemployment rate also stood at 6.1%, at the end of July, up 0.1 percentage points over the previous month (6%), according to the standards of the International Labor Bureau.

The annual inflation rate in the Eurozone has remained stable in August compared to July, at 0.2%, according to a preliminary estimate published on Wednesday by the European Statistics Office (Eurostat). According to Eurostat, in the month of August, the most significant price increases were seem in food, alcohol and cigarettes, which have posted an annual increase of 1.3%, compared to 1.4% in July, followed by services, which have seen an annual increase of 1.1%, compared to 1.2% seen in July. On the other hand, energy prices have seen an annual decrease of 5.7% in August, compared to a decline of 6.7% seen in July. Eurostat had previously announced that in July, compared to June 2016, annual inflation dropped in nine EU member countries, has remained stable in seven countries and has increased in 12 states, including Romania, according to Agerpres. Eurostat has also announced on Wednesday that in July 2016, compared to June 2016, the unemployment rate has remained stable at 10.1% in the Eurozone, while in the European Union the unemployment rate has remained stable at 8.6%. Among the member states, the highest unemployment rates were seen in Greece, (23.5% in May 2016) and Spain (19.6%). On the opposite is Malta, with an unemployment rate of 3.9%, Czech Republic and Germany, both with 4.2%. Romania is below the EU average, with an unemployment rate of 6.1%. Compared to the situation in July 2015, the unemployment rate decreased in 24 member states, including Romania, has remained stable in Denmark and has increased in Estonia, Austria and Belgium. In Romania's case, according to data notified by the National Statistics Institute, (INS), the annual inflation has remained in negative territory in July as well, at -0.8%, down from -0.7% in June. Calculated based on the harmonized consumer price index, the drop has been -0.3%, the INS states. The seasonally adjusted unemployment rate also stood at 6.1%, at the end of July, up 0.1 percentage points over the previous month (6%), according to the standards of the International Labor Bureau.Thursday, September 1, 2016

France wants the EU to stop its negotiations with the US for a free-trade agreement.

"That means the end" of the talks, not a suspension, he said, adding he would officially make the demand at an EU trade minister meeting at the end of September.

"There is no political backing by France to these negotiations anymore," Fekl told RMC radio and BFM TV, even though the Europeans can continue to negotiate "until the end of time [because] nobody can legally oppose it".

Fekl said that TTIP talks were "obscure" and that that the US "gives nothing or just crumbles".

"That is not how you negotiate between equals and allies," he said, adding that it was not the EU commission's fault.

The French minister's declaration comes two days after German vice-chancellor Sigmar Gabriel said that TTIP talks had "de facto failed, even though nobody is really admitting it."

The EU commission, for its part, said on Monday that the "ball keeps rolling". Their chief negotiator Ignacio Garcia Bercero had also said that news of TTIP's demise was "greatly exaggerated".

Sunday, August 28, 2016

The drama of Brexit may soon be matched or eclipsed by crystallizing events in France, where the Long Slump is at last taking its political toll. A democracy can endure deflation policies for only so long. The attrition has wasted the French centre-right and the centre-left by turns, and now threatens the Fifth Republic itself. The maturing crisis has echoes of 1936, when the French people tired of 'deflation decrees' and turned to the once unthinkable Front Populaire, smashing what remained of the Gold Standard. Former Gaulliste president Nicolas Sarkozy has caught the headlines this week, launching a come-back bid with a package of hard-Right policies unseen in a western European democracy in modern times. But the uproar on the Left is just as revealing. Arnaud Montebourg, the enfant terrible of the Socialist movement, has launched his own bid for the Socialist Party with a critique of such ferocity that it bears examination.

The drama of Brexit may soon be matched or eclipsed by crystallizing events in France, where the Long Slump is at last taking its political toll. A democracy can endure deflation policies for only so long. The attrition has wasted the French centre-right and the centre-left by turns, and now threatens the Fifth Republic itself. The maturing crisis has echoes of 1936, when the French people tired of 'deflation decrees' and turned to the once unthinkable Front Populaire, smashing what remained of the Gold Standard. Former Gaulliste president Nicolas Sarkozy has caught the headlines this week, launching a come-back bid with a package of hard-Right policies unseen in a western European democracy in modern times. But the uproar on the Left is just as revealing. Arnaud Montebourg, the enfant terrible of the Socialist movement, has launched his own bid for the Socialist Party with a critique of such ferocity that it bears examination.Saturday, August 27, 2016

France has a host of home-grown economic woes that have nothing to do with the EU. The social model is funded by punitive taxes on employing labour, creating one of the worst 'tax wedges' in the world. A quarter of French aged 60-64 are in work – compared with 40pc for the OECD average – due to early retirement incentives. The state consumes 56pc of GDP, a Nordic level without Nordic labour flexibility. There are 360 separate taxes, some predating the revolution. Trade unions have a legal lockhold on companies with over 50 employees, yet command 7pc of membership. "It is an inferno that sadly lacks the poetry of Dante," says Prof Brigitte Granville, a french economist at Queen Mary University London.

France has a host of home-grown economic woes that have nothing to do with the EU. The social model is funded by punitive taxes on employing labour, creating one of the worst 'tax wedges' in the world. A quarter of French aged 60-64 are in work – compared with 40pc for the OECD average – due to early retirement incentives. The state consumes 56pc of GDP, a Nordic level without Nordic labour flexibility. There are 360 separate taxes, some predating the revolution. Trade unions have a legal lockhold on companies with over 50 employees, yet command 7pc of membership. "It is an inferno that sadly lacks the poetry of Dante," says Prof Brigitte Granville, a french economist at Queen Mary University London.Thursday, August 25, 2016

List of stocks that have been upgraded by Merril Lynch

1. Marathon Oil Corp. (NYSE: MRO) to a buy from neutral, with a price target of $21, which is higher than the $18 consensus of various analysts. The new target price implies a gain of more than 33% from the current price of $15.7.

2. Noble Corporation PLC (NYSE: NE) from underweight to neutral. However, the target price of the stock is unchanged at $7.5, which is below the consensus target price of $8. The stock closed at $6.39 hitting a new multi-year low.

3. Patterson-UTI Energy Inc. (NASDAQ: PTEN) to neutral from underperform. The new target price on the stock is $22, whereas the consensus target price is also the same. The stock closed at $19.96.

4. Sasol LTD. (NYSE: SSL) to a buy from an earlier rating of neutral. While the consensus target price of the stock is $32.09, the stock closed the day at $27.71.

5. Devon Energy Corp. (NYSE: DVN) makes it to the US 1 list of top ideas for Merrill.

Notwithstanding, the valuations of the energy sector at 40 times its forward price-to-earnings (P/E) is more than double to the S&P 500’s forward P/E of 17, according to Yardeni Research.

Though the Merrill Lynch report agrees that “energy looks expensive on depressed earnings,” they believe that “higher oil prices should drive higher earnings estimates. Investors are still underweight the sector and the sector’s weight in the S&P 500 has fallen to historically bullish levels”.

Wednesday, August 24, 2016

Elderly Germans may have to keep working until the age of 69 if a Bundesbank proposal is adopted.

It says Berlin should consider raising the retirement age to that level by 2060, from around 65 at the moment. The central bank says that otherwise the country may struggle to honour its pension commitments. It points out that the state pension system is in good financial health at present, but will come under pressure in coming decades. The Bundesbank says that as baby-boomers - those born in the post-World War Two period - retire, there will be fewer younger workers to replace them.. The retirement age for Germans is set to rise gradually to 67 by 2030. However, the bank believes that from 2050 this increase will not be enough for the German government to keep state pensions at their target level of at least 43% of the average income. It is therefore proposing pushing the retirement age up to 69. "Further changes are unavoidable to secure the financial sustainability (of the state pension system)," the Bundesbank said in its monthly report. But German government spokesman Steffen Seibert said they stood by retirement at 67. "Retirement at 67 is a sensible and necessary measure given the demographic development in Germany. That's why we will implement it as we agreed - step by step," he added.

Tuesday, August 23, 2016

You can see the oil industry's woes for yourself, at anchor in the Firth of Forth. Very Large Crude Carriers are parked off the coast of East Lothian until the price rises, full of North Sea oil recently loaded through the Hound Point terminal. Onshore storage facilities are full. You can see other tankers at rest and laden with the crude stuff off the coasts of Suffolk and Cornwall. The gamble made by oil traders is that the cost of storing oil in these tankers - two million barrels in each of the larger ones - is less than the gain to be made out of waiting to sell it. But industry hopes of a rise in the oil price have been dashed time and time again over the past two years. Other consequences can be seen over the horizon, on Shell platforms, where Wood Group maintenance workers are back on strike this coming week, in protest at the sharp cut to their pay. Others have protested at the change to rotas, shifting from two-week turnarounds to three-weeks. The consequences were also clear from another grim week for the oil and gas industry, as the majors unloaded their half year results. The message was consistent, and no reassurance to those offshore workers facing diminished pay and conditions - the cost-cutting goes on. As the results were published, the oil price fell yet again. Brent crude fell below $43, down 20% from a peak it reached in early June. With global supply still buoyant, the short-term expectation is for a continued fall, even if those tankers at anchor in the Forth are a sign of expectations that the price will pick up again before too long. In Britain, it is no compensation for the oil industry that the dollar value appear more attractive in pounds, following the weakening of sterling. The industry thinks, invests, accounts and reports in US dollars. The exchange rate becomes an issue when it reaches the customer. That rise in the sterling price for a given dollar rate represents the increased cost, for those who earn and invest and buy their fuel in pounds - businesses and households alike.

You can see the oil industry's woes for yourself, at anchor in the Firth of Forth. Very Large Crude Carriers are parked off the coast of East Lothian until the price rises, full of North Sea oil recently loaded through the Hound Point terminal. Onshore storage facilities are full. You can see other tankers at rest and laden with the crude stuff off the coasts of Suffolk and Cornwall. The gamble made by oil traders is that the cost of storing oil in these tankers - two million barrels in each of the larger ones - is less than the gain to be made out of waiting to sell it. But industry hopes of a rise in the oil price have been dashed time and time again over the past two years. Other consequences can be seen over the horizon, on Shell platforms, where Wood Group maintenance workers are back on strike this coming week, in protest at the sharp cut to their pay. Others have protested at the change to rotas, shifting from two-week turnarounds to three-weeks. The consequences were also clear from another grim week for the oil and gas industry, as the majors unloaded their half year results. The message was consistent, and no reassurance to those offshore workers facing diminished pay and conditions - the cost-cutting goes on. As the results were published, the oil price fell yet again. Brent crude fell below $43, down 20% from a peak it reached in early June. With global supply still buoyant, the short-term expectation is for a continued fall, even if those tankers at anchor in the Forth are a sign of expectations that the price will pick up again before too long. In Britain, it is no compensation for the oil industry that the dollar value appear more attractive in pounds, following the weakening of sterling. The industry thinks, invests, accounts and reports in US dollars. The exchange rate becomes an issue when it reaches the customer. That rise in the sterling price for a given dollar rate represents the increased cost, for those who earn and invest and buy their fuel in pounds - businesses and households alike.Monday, August 22, 2016

Investors’ love for bonds continued in July, with intermediate-term bonds seeing an inflow of $15 billion for the month — the largest inflow of any Morningstar category. Intermediate-term bonds, which have gained 4.74% the past 12 months, have led Morningstar’s monthly report for the past five months. At the same time, investors — mainly with advisers at their sides — yanked $27.3 billion from U.S. stock funds and $5.3 billion from international stock funds. For the most part, investors seem to be driven by fear, not greed, said Todd Rosenbluth, director of ETF and mutual fund research at S&P Global Market Intelligence. “There’s a nervousness among investors, given that we’re in the 8th year of a bull market,” Mr. Rosenbluth said. Rotating into investment-grade corporates isn’t exactly a daring move. “Verizon, ATT, General Electric are all doing fine.” Investors also seem to be less convinced that passively managed fixed income funds are better than actively managed ones, Mr. Rosenbluth said, despite the fact that any supporting data for active management is “mixed at best.” Investors put $13.5 billion into actively managed bond funds, vs. $20.5 billion for passively managed once. In contrast, investors pulled $32.9 billion from actively managed stock funds and added $33.8 billion to actively managed stock funds. The big worry is whether investors are seeking riskier types of bonds in their search for yield. Unfortunately, the answer seems to be “yes.” High-yield bonds, which have returned an average 13.59% this year, saw a $3.2 billion inflow in July. Emerging-markets bond funds saw a $2.9 billion inflow. Those funds have gained 12.88% this year. Rising interest rates could short-circuit any bond rally, although that doesn’t seem to be a danger in Europe, where the economy is still stagnant. But both high-yield funds and emerging-markets funds could take significant hits if the U.S. or world economy falls further.

Investors’ love for bonds continued in July, with intermediate-term bonds seeing an inflow of $15 billion for the month — the largest inflow of any Morningstar category. Intermediate-term bonds, which have gained 4.74% the past 12 months, have led Morningstar’s monthly report for the past five months. At the same time, investors — mainly with advisers at their sides — yanked $27.3 billion from U.S. stock funds and $5.3 billion from international stock funds. For the most part, investors seem to be driven by fear, not greed, said Todd Rosenbluth, director of ETF and mutual fund research at S&P Global Market Intelligence. “There’s a nervousness among investors, given that we’re in the 8th year of a bull market,” Mr. Rosenbluth said. Rotating into investment-grade corporates isn’t exactly a daring move. “Verizon, ATT, General Electric are all doing fine.” Investors also seem to be less convinced that passively managed fixed income funds are better than actively managed ones, Mr. Rosenbluth said, despite the fact that any supporting data for active management is “mixed at best.” Investors put $13.5 billion into actively managed bond funds, vs. $20.5 billion for passively managed once. In contrast, investors pulled $32.9 billion from actively managed stock funds and added $33.8 billion to actively managed stock funds. The big worry is whether investors are seeking riskier types of bonds in their search for yield. Unfortunately, the answer seems to be “yes.” High-yield bonds, which have returned an average 13.59% this year, saw a $3.2 billion inflow in July. Emerging-markets bond funds saw a $2.9 billion inflow. Those funds have gained 12.88% this year. Rising interest rates could short-circuit any bond rally, although that doesn’t seem to be a danger in Europe, where the economy is still stagnant. But both high-yield funds and emerging-markets funds could take significant hits if the U.S. or world economy falls further.Sunday, August 21, 2016

Oil charges into bull market territory on hopes of output freeze Brent crude charged into bull market territory, smashing $50 a-barrel, as the world’s biggest oil producers prepared to discuss a possible output freeze at next month’s Opec meeting in an attempt to curb the global supply glut.Since hitting a low of $41.69 on August 3, oil has rallied almost 22pc, touching an intraday high of $50.87 yesterday - its highest level since July 4 when it touched $51.29. The latest leg up in the black stuff is pinned on the hopes that Opec’s meeting in Algeria on September 26 to 28, which takes place on the sidelines of the International Energy Forum, will revive talks on freezing production levels to help bolster prices. It was also lifted by the weak dollar which makes commodities cheaper for other currency holders. However, the oil price bounce comes less than three weeks after it fell into bear market territory, having fallen by more than 20pc from June 8 to July 29 amid oversupply concerns and pressures about slowing economic growth. Joshua Mahony, of IG, cautioned: “Given that this market turned higher almost instantaneously after confirming a bear market earlier in the month, perhaps this definition should be something to worry about rather than drive enthusiasm.”

The return of the bulls prompted oil majors to make gains, BP rose 2.8p at 435.6p, Tullow Oil climbed 5.5p to 239.6p and Amec Foster Wheeler advanced 13.5p to 540.5p.

Subscribe to:

Posts (Atom)