"DRAGHI SAYS EU BUDGET RULES ARE THERE TO BE RESPECTED" - Draghi also realises that big countries will ignore them with impugnity - just like they did the first time around. France is already in violation and knows full well that the EU and the ECB are utterly importent in the face of that. Just as they were when Germany - yes, Germany - lead the way in breaking the rules shortly after the euro came into being. All countries remember this, espescially the ones on the receiving end of imperious Germanic lectures about "doing their homework". Germany has made the classic mistake of doing well when others around it are doing badly, presuming this state of affairs will persist eternally and feeling it has a free hand to treat it's neighbours as it pleases. The moment German needs demand it, the Fiscal Pact will be out of the window; Anegla Merkel would be out of office within weeks if her government were to attempt the sort of austerity it has, in essence, forced upon Greece. The Netherlands were, if anything, even more hawkish than the Germans regarding "lazy Southerners" and wanted things like automatic fines. Then their own economy began to suffer the same problems and they also breached the rules - you don't hear much from them these days. Our Scottish friends may wish to ponder the huge difference in the treatment meted out to small countries as opposed to large ones in the EU. Of course, none of this should be greeted with any Satisfaction in the UK. A recession in the eurozone is bad for us too. Though thankfuly we have at least managed to dodge the madness of dropping a hand-grenade into the economy via a Scottish separation. Now, a worsening recession means there will be less taxable income for governments to fund ever growing entitlements. Add that to a huge pile of moldering away bad debts. What I see is not a solvable problem the way the world works today.

"DRAGHI SAYS EU BUDGET RULES ARE THERE TO BE RESPECTED" - Draghi also realises that big countries will ignore them with impugnity - just like they did the first time around. France is already in violation and knows full well that the EU and the ECB are utterly importent in the face of that. Just as they were when Germany - yes, Germany - lead the way in breaking the rules shortly after the euro came into being. All countries remember this, espescially the ones on the receiving end of imperious Germanic lectures about "doing their homework". Germany has made the classic mistake of doing well when others around it are doing badly, presuming this state of affairs will persist eternally and feeling it has a free hand to treat it's neighbours as it pleases. The moment German needs demand it, the Fiscal Pact will be out of the window; Anegla Merkel would be out of office within weeks if her government were to attempt the sort of austerity it has, in essence, forced upon Greece. The Netherlands were, if anything, even more hawkish than the Germans regarding "lazy Southerners" and wanted things like automatic fines. Then their own economy began to suffer the same problems and they also breached the rules - you don't hear much from them these days. Our Scottish friends may wish to ponder the huge difference in the treatment meted out to small countries as opposed to large ones in the EU. Of course, none of this should be greeted with any Satisfaction in the UK. A recession in the eurozone is bad for us too. Though thankfuly we have at least managed to dodge the madness of dropping a hand-grenade into the economy via a Scottish separation. Now, a worsening recession means there will be less taxable income for governments to fund ever growing entitlements. Add that to a huge pile of moldering away bad debts. What I see is not a solvable problem the way the world works today.

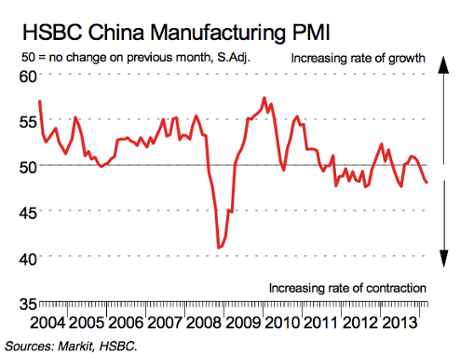

Neither Draghi or any of the bankers even bother to talk about the real problem of not enough regional income and too much government spending. Draghi’s only solution is some form of money printing. Printing money to pay bills might work over the short term. But long term, it cannot. If money printing works in the real world why not print and give every one a billion dollars, euros or yen?

The most Draghi can do is have the ECB print money to service existing bad debts made by banks and governments. But printing money to pay interest and principle on loans is not debt service. That is called money printing, debasing the currency whatever. Yes, governments want to do whatever possible to avoid bad times for its citizens. But, as someone else once said, the road to hell is paved with good intentions.