Spain’s constitutional court has moved to stop the Catalan government making a unilateral declaration of independence by suspending the regional parliament session in which the results of Sunday’s referendum were due to be discussed. On Thursday, the court upheld a challenge by Catalonia’s Socialist party – which opposes secession from Spain – ruling that allowing the Catalan parliament to meet on Monday and potentially declare independence would violate the rights of the party’s MPs. Catalonia's political turmoil prompting firms to consider relocating . Banks Sabadell and Caixa among first to respond amid fears about access to rest of Spain and EU if independence is declared The court warned that any session carried out in defiance of its ban would be “null”, and added that the parliament’s leaders could face criminal action if they ignored the court order. Carme Forcadell, president of the Catalan parliament, said Monday’s session had not yet been formally convened, but that the court’s decision to suspend it “harms freedom of expression and the right of initiative of members of this parliament and shows once more how the courts are being used to solve political problems.” The Catalan government is understood to be meeting to discuss its response to the latest move by the court. It has previously ignored the constitutional court’s rulings, not least its order to suspend the referendum itself. In a television address on Wednesday evening, the Catalan president, Carles Puigdemont, repeated his calls for mediation and dialogue with the Spanish government, but said the results of the vote would be put before parliament. “On Sunday we had a referendum under the most difficult circumstances and set an example of who we are,” he said. “Peace and accord is part of who we are. We have to apply the results of the referendum. We have to present the results of the referendum to parliament.”

Spain’s constitutional court has moved to stop the Catalan government making a unilateral declaration of independence by suspending the regional parliament session in which the results of Sunday’s referendum were due to be discussed. On Thursday, the court upheld a challenge by Catalonia’s Socialist party – which opposes secession from Spain – ruling that allowing the Catalan parliament to meet on Monday and potentially declare independence would violate the rights of the party’s MPs. Catalonia's political turmoil prompting firms to consider relocating . Banks Sabadell and Caixa among first to respond amid fears about access to rest of Spain and EU if independence is declared The court warned that any session carried out in defiance of its ban would be “null”, and added that the parliament’s leaders could face criminal action if they ignored the court order. Carme Forcadell, president of the Catalan parliament, said Monday’s session had not yet been formally convened, but that the court’s decision to suspend it “harms freedom of expression and the right of initiative of members of this parliament and shows once more how the courts are being used to solve political problems.” The Catalan government is understood to be meeting to discuss its response to the latest move by the court. It has previously ignored the constitutional court’s rulings, not least its order to suspend the referendum itself. In a television address on Wednesday evening, the Catalan president, Carles Puigdemont, repeated his calls for mediation and dialogue with the Spanish government, but said the results of the vote would be put before parliament. “On Sunday we had a referendum under the most difficult circumstances and set an example of who we are,” he said. “Peace and accord is part of who we are. We have to apply the results of the referendum. We have to present the results of the referendum to parliament.”

Access Investments-Building Awareness - European Union-ROMANIA

Showing posts with label Spania. Show all posts

Showing posts with label Spania. Show all posts

Saturday, October 7, 2017

Spain’s constitutional court has moved to stop the Catalan government making a unilateral declaration of independence by suspending the regional parliament session in which the results of Sunday’s referendum were due to be discussed. On Thursday, the court upheld a challenge by Catalonia’s Socialist party – which opposes secession from Spain – ruling that allowing the Catalan parliament to meet on Monday and potentially declare independence would violate the rights of the party’s MPs. Catalonia's political turmoil prompting firms to consider relocating . Banks Sabadell and Caixa among first to respond amid fears about access to rest of Spain and EU if independence is declared The court warned that any session carried out in defiance of its ban would be “null”, and added that the parliament’s leaders could face criminal action if they ignored the court order. Carme Forcadell, president of the Catalan parliament, said Monday’s session had not yet been formally convened, but that the court’s decision to suspend it “harms freedom of expression and the right of initiative of members of this parliament and shows once more how the courts are being used to solve political problems.” The Catalan government is understood to be meeting to discuss its response to the latest move by the court. It has previously ignored the constitutional court’s rulings, not least its order to suspend the referendum itself. In a television address on Wednesday evening, the Catalan president, Carles Puigdemont, repeated his calls for mediation and dialogue with the Spanish government, but said the results of the vote would be put before parliament. “On Sunday we had a referendum under the most difficult circumstances and set an example of who we are,” he said. “Peace and accord is part of who we are. We have to apply the results of the referendum. We have to present the results of the referendum to parliament.”Monday, October 2, 2017

Wednesday, January 6, 2016

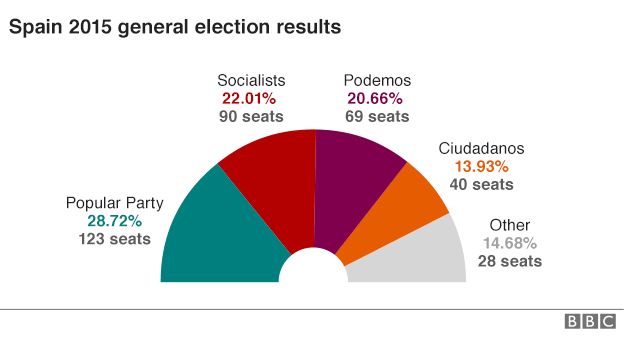

Spain's left-wing Podemos (We Can) party has refused to join any coalition led by the centre-right Popular Party (PP), which won the 20 December election but fell short of a majority.

Podemos was launched nearly two years ago, based on mass anti-austerity protests. It came third, with 69 seats. Podemos leader Pablo Iglesias rebuffed the PP leader and acting Prime Minister Mariano Rajoy, as did the Socialist (PSOE) leader Pedro Sanchez last week. New elections might have to be held. The PP came top with 123 seats in the 350-seat lower house of parliament - far short of a majority. In second place was the PSOE with 90, and the new liberal Ciudadanos (Citizens) party was fourth with 40. Speaking after talks with Mr Rajoy, Mr Iglesias his priority was "social emergency" legislation to help families threatened with eviction and other socially vulnerable groups, such as poor pensioners. He refused to support Mr Rajoy "whether actively or passively" - ruling out a coalition partnership or abstention in a confidence vote.

Ciudadanos leader Albert Rivera also told Mr Rajoy he would not back him. But Ciudadanos would abstain in the confidence vote if Mr Rajoy managed to put together a coalition, he said.

The PSOE says it will only consider a leftist coalition with Podemos if the latter drops its support for an independence referendum in Catalonia. Many Catalans want such a referendum, but Podemos is the only one of Spain's major parties to back the idea. Mr Sanchez called on Podemos to "renounce any position that implies the rupture of co-existence between Spaniards". Next month King Felipe VI will seek to nominate a party leader for government, but that leader must then win a vote of confidence in parliament. If there is deadlock two months after that the king will call a fresh election.

Tuesday, June 2, 2015

The sooner this failed experiment collapses in a heap the better...

It is funny , isn't it ? The 'experts' (hacks) keep writing stories predicting the end of the Euro and mass default causing catastrophic financial mayhem, yet still it continues and the Spanish government is looking for ways to prop it up. So we see that NOTHING will derail the corrupt scam which is 'The EU'....5000 years ago man started building temples and worshiping some deity to make the rains come and the harvest good. Today we do the same only we appoint our deities and pray to them to make inflation low and employment high. Never mind that monetary policy, like the rains, can only create favorable conditions for economic growth but it cannot create it. Regulatory environments, tax policy and those old ingredients of capital, labor and technology have to be planted to get a harvest. Worshiping at the temple of Mammon only goes so far... 28 countries, each with its own national identity, each wanting something different from the EU, each with its own fiscal requirements. No wonder the EU is pulling itself apart. The sooner this failed experiment collapses in a heap the better....The people with the blinkers are those with their snouts in the Brussels trough, blind to what is actually happening in the good countries of Europe. The peoples of these sovereign nations are not melding into obedient 'Europeans' They are proud citizens of their home countries, and they are getting angrier by the day. If the freeloading elite don't come to their senses soon there is a real risk of violence, which is why idiots like you need to drop your stupid European fantasies and look to see which way the wind is blowing..

It is funny , isn't it ? The 'experts' (hacks) keep writing stories predicting the end of the Euro and mass default causing catastrophic financial mayhem, yet still it continues and the Spanish government is looking for ways to prop it up. So we see that NOTHING will derail the corrupt scam which is 'The EU'....5000 years ago man started building temples and worshiping some deity to make the rains come and the harvest good. Today we do the same only we appoint our deities and pray to them to make inflation low and employment high. Never mind that monetary policy, like the rains, can only create favorable conditions for economic growth but it cannot create it. Regulatory environments, tax policy and those old ingredients of capital, labor and technology have to be planted to get a harvest. Worshiping at the temple of Mammon only goes so far... 28 countries, each with its own national identity, each wanting something different from the EU, each with its own fiscal requirements. No wonder the EU is pulling itself apart. The sooner this failed experiment collapses in a heap the better....The people with the blinkers are those with their snouts in the Brussels trough, blind to what is actually happening in the good countries of Europe. The peoples of these sovereign nations are not melding into obedient 'Europeans' They are proud citizens of their home countries, and they are getting angrier by the day. If the freeloading elite don't come to their senses soon there is a real risk of violence, which is why idiots like you need to drop your stupid European fantasies and look to see which way the wind is blowing..Saturday, May 30, 2015

Europe faces the risk of a second revolt by Left-wing forces in the South after Spain's, Portugal’s Socialist Party vowed to defy austerity demands from the country’s creditors and block any further sackings of public officials. "We will carry out a reverse policy,” said Antonio Costa, the Socialist leader. Mr Costa said a clear majority of his party wants to halt the “obsession with austerity”. Speaking to journalists in Lisbon as his country prepares for elections - expected in October - he insisted that. Portugal must start rebuilding key parts of the public sector following the drastic cuts under the previous EU-IMF Troika regime. The Socialists hold a narrow lead over the ruling conservative coalition in the opinion polls and may team up with far-Left parties, possibly even with the old Communist Party. “There must be an alternative that allows us to turn the page on austerity, revive the economy, create jobs, and – while complying with euro area rules – restore hope to this county,” he said. The plan would appear entirely incompatible with the EU’s Fiscal Compact, which requires Portugal to run massive primary surpluses to cut its public debt from 130pc to 60pc of GDP over 20 years under pain of sanctions. The increasingly fierce attacks on austerity in Lisbon are likely to heighten fears in Berlin that fiscal and reform discipline will break down altogether in southern Europe if Greece’s rebels win concessions. Worry about political "moral hazard" is vastly complicating the search for a solution in Greece. “Greece is the testing ground and everybody is watching very carefully. That is why the Spanish and Portuguese prime ministers have been so hawkish,” said Vincenzo Scarpetta, from Open Europe.

Europe faces the risk of a second revolt by Left-wing forces in the South after Spain's, Portugal’s Socialist Party vowed to defy austerity demands from the country’s creditors and block any further sackings of public officials. "We will carry out a reverse policy,” said Antonio Costa, the Socialist leader. Mr Costa said a clear majority of his party wants to halt the “obsession with austerity”. Speaking to journalists in Lisbon as his country prepares for elections - expected in October - he insisted that. Portugal must start rebuilding key parts of the public sector following the drastic cuts under the previous EU-IMF Troika regime. The Socialists hold a narrow lead over the ruling conservative coalition in the opinion polls and may team up with far-Left parties, possibly even with the old Communist Party. “There must be an alternative that allows us to turn the page on austerity, revive the economy, create jobs, and – while complying with euro area rules – restore hope to this county,” he said. The plan would appear entirely incompatible with the EU’s Fiscal Compact, which requires Portugal to run massive primary surpluses to cut its public debt from 130pc to 60pc of GDP over 20 years under pain of sanctions. The increasingly fierce attacks on austerity in Lisbon are likely to heighten fears in Berlin that fiscal and reform discipline will break down altogether in southern Europe if Greece’s rebels win concessions. Worry about political "moral hazard" is vastly complicating the search for a solution in Greece. “Greece is the testing ground and everybody is watching very carefully. That is why the Spanish and Portuguese prime ministers have been so hawkish,” said Vincenzo Scarpetta, from Open Europe. Monday, May 25, 2015

Compromises and coalitions between parties is new in Spain where more than 30 years of alternating power between the socialists and the conservatives is being challenged by an increasingly fragmented political system including anti-austerity party Podemos and centrist Ciudadanos.

Compromises and coalitions between parties is new in Spain where more than 30 years of alternating power between the socialists and the conservatives is being challenged by an increasingly fragmented political system including anti-austerity party Podemos and centrist Ciudadanos.

The biggest changes have been the move towards the new left parties in Barcelona and maybe also in Madrid - depending on a possible pact between a Podemos-supporting coalition called Ahora Madrid and the Social Democrats (PSOE). It would be the first time the Spanish capital would have a leftwing Mayor in the last 25 years. “It is clear that a majority for change has won,” said Manuela Carmena, the 71 year-old emeritus judge of the Spanish Supreme Court who wants to become Madrid’s new mayor. She is one seat short of Madrid’s former conservative Mayor Esperanza Aguirre. However, with the support of Social Democrats – who came third - the left-wing parties could together hold the absolute majority in Madrid. Barcelona’s new Mayor Ada Colau calls for “more social justice” and leads a coalition of left-wing parties and citizens’ organisations called ‘Barcelona en Comú’, which includes members of Podemos.

“We are proud that this process hasn’t just been an exception in Barcelona, this is an unstoppable democratic revolution in Catalonia, in [Spain] and hopefully in southern Europe,” Colau said last night after it became clear that she had won a small majority in the Catalan capital.

Colau, a former anti-eviction activist, was one of the founders of a platform for people affected by mortgages - Plataforma Afectados por la Hipoteca (PAH) - which won the European Parliament’s European Citizens’ Prize in 2013. The PAH was set up in response to the hike in evictions caused by abusive mortgage clauses during the collapse of the Spanish property market eight years ago. Colau herself entered politics last year calling for “more and better democracy” and a clean-up of corruption in politics. “It is the end of bipartisanship,” Podemos leader and MEP Pablo Iglesias said on Sunday. “May this Spring bring us flying to November”, he added on Twitter, referring to the Spanish general election. Together, the two mainstream parties PP and PSOE represented 51 percent of the votes yesterday - much less than the 65 percent four years ago. Centrist party Ciudadanos was the third most voted party although not as big a force as polls had expected. However, the party will hold a kingmaker role in many municipalities and in minimum three regions.

Although Podemos comes in as the fourth most voted party, the party’s real success has been merging with other local grassroot parties also calling for social change. The social indignados movement - also called 15M movement - that camped out on the main squares across Spain in 2011 calling for a radical change in Spanish politics, has now turned into political representation. Sunday’s elections in the 13 out of 17 regions and in over 8000 municipalities is likely to be a preview of the results of the Spanish General election expected for the end of the year. Despite the Spanish economy picking up after years of an economic crisis, the former established parties are still being punished for the continuing high unemployment - especially among young people - and for corruption scandals that have marred their reputation. The necessary pacts and coalitions could lead to drawn out and complicated negotiations. In the southern region of Andalucia, which held elections in March, the socialist minority government has failed three times to secure the majority vote needed to form a government.

Monday, April 6, 2015

In southern Spain the Socialist party won a closely-watched regional election

in Andalucia, where it has governed since the restoration of Spanish democracy

in the 1980s. But Podemos from the radical left - the Spanish Syriza - won an impressive

15% of the vote; little more than a year after the party was formed. The big loser in Andalucia was the centre right People's Party, which runs

the government in Madrid, even though it came second overall. The PP will be particularly concerned because the threat to the status quo

doesn't come only from the left. An upstart centrist party, Ciudadanos, also won 9% of the vote, attracting

support from people disillusioned by business as usual. So where does this leave the two main parties in Spain? As recently as 2008, the Socialists and the PP between them won nearly 84% of

the vote in a general election. They won't come anywhere near that when the country goes to the polls later

this year. Podemos is still some way behind them. But it is indisputably on the

rise. But the FN still came second with more than 25% of the vote, pushing the

governing Socialists into third place. That suggests that support for the FN's anti-immigration, anti-EU message is

more than a simple protest vote. Even if the mainstream parties conspire to keep the FN out wherever they can

in the second round of voting, the French elections are another sign that many

disgruntled citizens are now ready and willing to look for alternatives. Elsewhere on the continent there are similar stories. The rise of the Five Star Movement in Italy or UKIP in the UK, or even the AfD (Alternative for

Germany) in Germany, suggest that some political fault lines are moving. The idea of a 'democratic deficit' has exercised many political minds,

particularly among supporters of the European Union. Parties like Syriza and Podemos want to redefine what the EU does. But many protest parties want to destroy it. Of course, the centre ground is not dead. Well-funded party machines do not disappear overnight (even if supporters of

the Greek Socialist party PASOK may beg to differ). But traditional parties across Europe are under pressure as never before in

recent memory. And European politics has become fascinatingly unpredictable.

In southern Spain the Socialist party won a closely-watched regional election

in Andalucia, where it has governed since the restoration of Spanish democracy

in the 1980s. But Podemos from the radical left - the Spanish Syriza - won an impressive

15% of the vote; little more than a year after the party was formed. The big loser in Andalucia was the centre right People's Party, which runs

the government in Madrid, even though it came second overall. The PP will be particularly concerned because the threat to the status quo

doesn't come only from the left. An upstart centrist party, Ciudadanos, also won 9% of the vote, attracting

support from people disillusioned by business as usual. So where does this leave the two main parties in Spain? As recently as 2008, the Socialists and the PP between them won nearly 84% of

the vote in a general election. They won't come anywhere near that when the country goes to the polls later

this year. Podemos is still some way behind them. But it is indisputably on the

rise. But the FN still came second with more than 25% of the vote, pushing the

governing Socialists into third place. That suggests that support for the FN's anti-immigration, anti-EU message is

more than a simple protest vote. Even if the mainstream parties conspire to keep the FN out wherever they can

in the second round of voting, the French elections are another sign that many

disgruntled citizens are now ready and willing to look for alternatives. Elsewhere on the continent there are similar stories. The rise of the Five Star Movement in Italy or UKIP in the UK, or even the AfD (Alternative for

Germany) in Germany, suggest that some political fault lines are moving. The idea of a 'democratic deficit' has exercised many political minds,

particularly among supporters of the European Union. Parties like Syriza and Podemos want to redefine what the EU does. But many protest parties want to destroy it. Of course, the centre ground is not dead. Well-funded party machines do not disappear overnight (even if supporters of

the Greek Socialist party PASOK may beg to differ). But traditional parties across Europe are under pressure as never before in

recent memory. And European politics has become fascinatingly unpredictable.Sunday, December 8, 2013

Ukraine's President Viktor Yanukovych

and his Russian counterpart Vladimir Putin have held surprise talks on a

"strategic partnership treaty". Mr Yanukovych flew from China to Sochi in southern Russia for the meeting. He

has also cancelled a visit to Malta.

Ukraine's President Viktor Yanukovych

and his Russian counterpart Vladimir Putin have held surprise talks on a

"strategic partnership treaty". Mr Yanukovych flew from China to Sochi in southern Russia for the meeting. He

has also cancelled a visit to Malta.

Last month he shelved a partnership deal with the EU, triggering angry

protests in Ukraine's capital Kiev.

In Sochi he discussed "preparation of a future treaty on strategic

partnership" with Russia, his press service said.

The talks covered various economic issues, the statement said, without

elaborating.

Thousands of anti-Yanukovych protesters remain outside the government

building on Kiev's Independence Square, braving bitter cold. They are furious that he made an 11th-hour U-turn in relations with the EU,

refusing to sign an association agreement that had been prepared during years of

negotiations.

Mr Putin has been urging Ukraine to join Russia's customs union with Belarus

and Kazakhstan - a union whose entry terms are far less demanding than the

EU's.

In recent months Russia has put Ukraine under economic pressure, imposing

long customs delays at the border and banning imports of Ukrainian sweets.

Monday, November 18, 2013

All EU budgets have to be approved by The Bundestag - did anyone know ???

Hopefully, in their blind obedience to Merkel and co, the amazingly stupid and corrupt EU Commission will have gone yet another step too far. If You are Italian or Spanish and you read the headline in your local paper that the EU wants to make you poorer and take more power to themselves from your Government.

I think ropes and lampposts are in order for the EU Commissioners if they go much further.

Spain and Italy have been warned that their budgets for 2014 are in breach of European Union rules as Brussels uses new powers to force governments to revise spending plans before national parliaments vote on them. France was also cautioned that plans for painful economic reforms represent only "limited progress" as the European Commission exercised new eurozone powers in a historic shift of sovereignty away from elected governments. "Because in an economic and monetary union, national budgetary decisions can have an impact well beyond national borders, member states have given the commission the responsibility," said Olli Rehn, the commission vice-president in charge of the euro.

"I trust that they will thus be taken on board by national decision makers." Germany, Europe's largest and most successful economy, was also criticized for making "no progress" in following EU recommendations to help its eurozone neighbors by spurring domestic demand and imports. Fabrizio Saccomanni, the Italian finance minister and a technocrat imposed on the Italian government at the behest of EU officials, could be fatally weakened by the Brussels intervention, especially after Mr Rehn ruled out an exempting €3bn in investment spending that the Italian government has included in its 2014 budget. Mr Saccomanni warned that Italy could not take the investment spending from the national budget to meet EU rules because the cut would threaten the country's already weak economic recovery and inflame opposition to austerity.

"We could have taken even more restrictive measures to reduce our public spending, but I imagine there would be even more cries of pain. I believe our approach is balanced," he said. "It is not necessary to change the budget." Spain was told that its "draft budgetary plan is at risk of non-compliance with the rules, as the headline deficit target may be missed and the recommended improvement in the structural balance is currently not expected to be delivered". France was given the green light on its budget but the commission warned that next year's budget leaves "no margin" for deviation and reforms "constitute limited progress" in addressing structural targets. "A significant set of measures on top of those already specified will be needed to ensure that the target for 2015 is reached," said the commission. The commission also cautioned Finland, Malta and Luxembourg, asking the three countries to review their 2014 budgets to ensure that they meet eurozone targets.

Sunday, November 10, 2013

Borrowers across the struggling eurozone economies received an unexpected fillip on Thursday when the European Central Bank cut interest rates to a fresh record low, in a bid to stave off a slide into deflation.

After its monthly policy meeting in Frankfurt, the ECB's governing council announced that it would reduce its key refinancing rate to 0.25%, from 0.5%. While the economy of the 18-member single currency area clambered out of recession earlier this year, Mario Draghi, the ECB's president, warned that the outlook could deteriorate in the coming months. "The risks surrounding the economic outlook for the euro area continue to be on the downside," he said. "Developments in global money and financial market conditions and related uncertainties may have the potential to negatively affect economic conditions. Other downside risks include higher commodity prices, weaker than expected domestic demand and export growth, and slow or insufficient implementation of structural reforms in euro area countries." As well as the rate cut, which took financial markets by surprise, Draghi said the ECB would continue making low-cost loans to eurozone banks until at least mid-2015, to try to prevent the financial sector from seizing up.

Howard Archer, of consultancy IHS Global Insight, said: "The fact that the ECB chose to act now rather than wait until December when the governing council will have the ECB staff's new eurozone GDP and consumer price inflation forecasts suggests that the bank felt there was a compelling case for prompt action."

With inflation running well below the ECB's 2% target, at just 0.7% in October, a growing number of analysts have started to warn that deflation – which can be disastrous for economies carrying a heavy debt burden, as prices and wages fall while debt-levels remain fixed – is a real threat. Draghi suggested at his press conference that, "we may experience a prolonged period of low inflation".

Friday, September 20, 2013

An Opera in Twenty Farts -- We have entered the period of fart diplomacy in the episode that will

become known as Obama's Syrian Farce. We all know that Freedman's account is

patently untrue. Putin discussed this possibility with Obama at the G20, and

Kerry, Muppet as he is, probably recalled something in his fried brain and

blurted it out. The idea that the world has been saved by a blunder, is the

disney version of the Syrian crisis that obviously appeals to hacks like

Freedland. Why that is so, I will leave you, dear colleague, to ponder.

An Opera in Twenty Farts -- We have entered the period of fart diplomacy in the episode that will

become known as Obama's Syrian Farce. We all know that Freedman's account is

patently untrue. Putin discussed this possibility with Obama at the G20, and

Kerry, Muppet as he is, probably recalled something in his fried brain and

blurted it out. The idea that the world has been saved by a blunder, is the

disney version of the Syrian crisis that obviously appeals to hacks like

Freedland. Why that is so, I will leave you, dear colleague, to ponder.

Fart diplomacy is that tactic used by Great World Leaders when they have been

caught with their pants down and their underwear is not, shall we say, what

their mothers would have wished. Its aim is to drown out the obvious judgments

of onlookers, such as "You've been had, you bunch of gits !", by making loud

rude noises and stinking up the air. "A little hair on my pinkie can destroy the

whole of your army with its arm tied behind its back ! God bless Mrka"

In reality God will do no such thing. Swayed between amusement and disgust,

God is wondering whether to perhaps inflict a plague of piles on Kerry and

Obama, as they swagger and posture like drunk children in a sandbox.

"Well., sure, this may work, but I am highly skeptical," says Grand Poopie

Obama, looking suitably skeptical. "See, there's a lot of things that will have

to be got right, and that will take time, and we dont have time, God Bless Mrka

!"

"Assad is famous for his lies,"shouts Kerry, and then "Shit, what bit me in

my ass ??!! God is that you biting me in my ass ?!! What did I do ? Told lies ?

OK, but hell, that was for the sake of Mrka !"

"Listen up, Assad, we are going to press on with getting permission to blow

Syrian babies to smithereens, regardless of what You and Mr Pootin have come up

with. So dont think you're off the hook, Adolph, We've got your number."

In Russia in the UN and in Syria, well intentioned diplomats are scuttling to

try to prevent the destruction by US tomahawks of thousands of mothers and

children, o, yes, and men too. Obaqmna never mentions men who have been

murdered. You've noticed that too ? Its not in the script. And while these

earnest. efforts are afoot, we get loud farting trombone sounds from the Rose

Garden of the White House. "This is too little too late. Assad's slaughter of his people must stop. Now

! "

Question from meek embedded reporter looking remarkably like Jonathan

Freedland, but that's just a coincidence (promise): "Mr Obama, do you have any

messages for the rebels who continue to slaughter Syrians in huge numbers ?"

The Great Poobear puts on suitable furrowed brow intended to display "deep

thought: " The Syrian people have had enough misery. The world is watching. I

cant stand idly by. This too must cease. Assad has killed more Syrians than

Adolf Hitler ! Hiccup. Burp"

And so it will go on for several days, this period of fart diplomacy, during

which the Leader of the Free World will discover a way of pulling up his pants

so he can strut, jaw out like Mussolini, to show the Mrkn people that they can

be proud to be Mrkn,.... again. Kerry ? Listen, Ive got a tip for you. Give it a few months and then go

around the trash cans in Farrgut Park across the road form the White House (that

Bastion of World Freedom and Democracy), and you may find Kerry in a can among

the Dr Pepper bottles.

Monday, August 5, 2013

Spanish GDP falls by 0.1% - Spain's economy has now been shrinking for two full years.

Spanish GDP falls by 0.1% - Spain's economy has now been shrinking for two full years.

Data just released by the Spanish National Statistics Institute showed that Spanish GDP fell by 0.1% between April and June. That's the eighth quarterly contraction in a row.

Encouragingly, though, the pace of decline has slowed -- following the 0.5% contraction suffered in the first three months of 2013.

And on a year-on-year basis, the Spanish economy has shrunk by 1.7%... well this is slightly better than the 1.8% economists had expected. I don't think we can call it a green shoot of recovery – but perhaps the bitter frost is easing?

In a statement on its

website, Bitcoin said it had given a presentation to the Bank of

Thailand about how the currency works in a bid to operate in the country.

However, at the end of the meeting, "senior members of the Foreign Exchange

Administration and Policy Department advised that due to lack of existing

applicable laws, capital controls and the fact that Bitcoin straddles multiple

financial facets... Bitcoin activities are illegal in Thailand". The ruling means it is illegal to buy and sell bitcoins, buy or sell any

goods or services in exchange for bitcoins, send any bitcoins to anyone outside

of Thailand, or receive bitcoins from anyone outside the country. Bitcoin said it "has no choice but to suspend operations until such as time

that the laws in Thailand are updated to account for the existance [sic] of

Bitcoin", adding that "the Bank of Thailand has said they will further consider

the issue, but did not give any specific timeline". Launched in 2009 in the wake of the global financial crisis, bitcoins are

"mined" using complex computer source code. The virtual currency started as a

relatively niche method of payment, devised by an anonymous programmer, but can

now be used for anything from online gambling to pizza delivery.

Saturday, July 27, 2013

In Spain ...a real tragedy..

As Spain mourned the 80 dead in Europe's worst rail crash this century, questions were being asked about how the train had been able to hit a tight curve at such a speed that it spun off into a concrete security wall. Analysis of video of the accident in the northern city of Santiago de Compostela suggested the train was going faster than 85mph on a bend where drivers are supposed to slow down after a straight stretch that allows them to reach up to 125mph. "We were going strongly when we got into the curve," one driver was reported to have admitted shortly after surviving the accident on Wednesday, which killed more than a third of the passengers and left 168 injured. A spokeswoman for the Galicia supreme court said the driver, who was only slightly injured, was under investigation. The man, who has been named, is not believed to be under arrest but is expected to face questions from a judge with access to the train's data recording black box.

As Spain mourned the 80 dead in Europe's worst rail crash this century, questions were being asked about how the train had been able to hit a tight curve at such a speed that it spun off into a concrete security wall. Analysis of video of the accident in the northern city of Santiago de Compostela suggested the train was going faster than 85mph on a bend where drivers are supposed to slow down after a straight stretch that allows them to reach up to 125mph. "We were going strongly when we got into the curve," one driver was reported to have admitted shortly after surviving the accident on Wednesday, which killed more than a third of the passengers and left 168 injured. A spokeswoman for the Galicia supreme court said the driver, who was only slightly injured, was under investigation. The man, who has been named, is not believed to be under arrest but is expected to face questions from a judge with access to the train's data recording black box.

While trapped in the cab, the driver was reported to have given an account over the radio to officials at Santiago station. He was quoted saying, "I hope there are no dead because they would fall on my conscience" and having repeated over and over: "We're human. We're human." Rail safety experts said such accidents are usually the result of more than one failure, and questions will inevitably be asked about how warning signals about the train's speed were not picked up and acted on. On Thursday evening the death count looked set to creep up, with 36 of the 95 victims in hospital said to be in a critical condition. One of the survivors, Sergio Prego, told Cadena Ser radio station that the train "travelled very fast" just before it derailed and the cars flipped upside down, on their sides and into the air. "I've been very lucky because I'm one of the few able to walk out," he said.

Forensic scientists were last night still trying to identify the most mutilated corpses. Groups of families and friends gathered at the city's Cersia hospital waiting for news of loved ones – though there was little chance they were alive as all survivors had been identified and their families informed.

"It's a major challenge to identify the people who have died," Rajoy said. "Unfortunately, in many cases, this isn't easy, but we are very conscious that the families cannot live in a state of uncertainty." The Alvia 730 series train started from Madrid and was scheduled to end its journey at Ferrol, about 60 miles north of Santiago. Alvias do not go as fast as Spain's AVE bullet trains, but still reach 155mph on AVE tracks and travel at a maximum 137mph on normal gauge rails. The accident came a day before a public holiday in Galicia: the feast of St James, after whom the region's capital Santiago is named. "24 July will no longer be the eve of a day of celebration but rather one commemorating one of the saddest days in the history of Galicia," said Alberto Núñez Feijóo, the region's president. Residents of the semi-rural neighbourhood by the accident site struggled to help victims out of the toppled cars on Wednesday night. Some passengers were pulled out of broken windows as rescuers used rocks to try to free survivors from the wreckage.

Wednesday, April 10, 2013

Spanish industrial production dives again - The economic crisis in Spain continues. Data released this morning showed that industrial production in the country tumbled by 6.5% in February, compared with a year ago.

Spanish industrial production dives again - The economic crisis in Spain continues. Data released this morning showed that industrial production in the country tumbled by 6.5% in February, compared with a year ago.

That's the 18th monthly contraction in a row.

The slump was driven by a double-digit decline in production of durable goods for consumers, who are suffering badly as Madrid implements its austerity programme.

But production was also down across the board, from other consumer goods to large-scale industrial equipment:

Many Spanish factories have closed since the financial crisis struck, creating a vicious circle of rising unemployment and falling demand.

One example, thousands of people were employed at a door factory in the town in Villacanas, south of Madrid. In the good days they churned out products for Spain's property boom - but the plant is now closed, along with most of of the Villacanas industrial park....

The picture is slightly better in France this morning, where industrial production only fell by 2.8% year-on-year in February, and actually picked up by 0.7% compared with January.

I'll be tracking the reaction to today's data, and watching developments across the eurozone -- particularly Slovenia (whose PM yesterday rejected speculation that a bailout would be needed), and Cyprus (where time is running out to agree its bailout).

Saturday, April 6, 2013

Excellent news ..."adios" investments in European Banks ....hahahaha...what an idiot !!!!

Plans from Brussels put the onus on bank depositors, rather than the taxpayer, to bear the costs of bank failures. "Cyprus was a special case ... but the upcoming directive assumes that investor and depositor liability will be carried out in case of a bank restructuring or a wind-down," Mr Rehn, the European Economic and Monetary Affairs Commissioner. "But there is a very clear hierarchy, at first the shareholders, then possibly the unprotected investments and deposits. However, the limit of €100,000 (£85,000) is sacred, deposits smaller than that are always safe." Mr Rehn was referring to a directive being drafted by the European Commission on bank safety which would set out investor liability in the law of member states. He was speaking in an interview with Finnish TV after Cyprus last month forced richer depositors to suffer heavy losses in order to secure a €10bn bail-out from the EU and the International Monetary Fund. ... Cyprus had initially planned to make people with deposits under the crucial €100,000 mark to take a cut also before performing backtracking in the face of an outcry. Smaller deposits are supposed to be protected by state guarantees. Mats Persson, director of think-tank Open Europe said: "Rehn was only re-stating what's in an EU proposal tabled in 2012, which quite sensibly suggests a mechanism whereby first, investors and secondly, large depositors - rather than taxpayers - foot the bill when a bank goes bust. “However, there's so much uncertainty around the precedent set by the Cyprus bail-out that his comments may still cause some jitters." Mr Rehn also said that the European Central Bank should launch fresh action to help boost the recession-hit euro zone economy....

Tuesday, March 26, 2013

Nigel Farage tonight-Get your money out of europe-BANK RUN, NOW !!!!

Nigel Farage tonight-Get your money out of europe-BANK RUN

“I must say the thing I

find the shabbiest about it is there insisting that it doesn’t need to be

subjected to a vote in the Cypriot Parliament. I very much hope that the

members of the Cypriot Parliament say, ‘To hell with that, we demand another

vote.’

It’s funny isn’t it, the

Germans are going to have a vote on it in their Parliament, but the Cypriots

are being told that they shouldn’t have a vote on it. If that’s not moving into

a German dominated Europe, I don’t know what is.

I said last week that I

felt any savers who had money in other eurozone banks, particularly in the

Southern eurozone countries, really ought to think seriously about getting

their money out. Well, this afternoon something far more serious has happened.

The Dutch Finance Minister, about an hour and a half ago, said that he saw the

Cyprus eurozone bailout as now being a template of how they intend to act in

the future. So the burden of all of this will now fall on the private sector,

and not on the public sector.

Frankly, what that now

says is that anybody that has money, or anybody that has big money sitting in a

Spanish or an Italian bank, and particularly if you happen to be a financial

officer for a company, it would be criminally negligent of you to now leave

your money or a company’s money in a Spanish or an Italian bank.

I think what they’ve

done today is to spark a major run on those banks. I see that some of the banks

stocks have fallen 6% this afternoon, and I think in their desperation to keep

the eurozone propped-up, I really believe that long-term they have made an

absolutely fatal error. They have now crossed the bounds into one of complete

criminality, and from this their reputations will never, ever recover.”

Monday, March 11, 2013

Mark Zandi, the chief economist of Moody's Analytics, said: "The job market remains sturdy in the face of significant fiscal headwinds. Businesses are adding to payrolls more strongly at the start of 2013 with gains across all industries and business sizes. Tax increases and government spending cuts don't appear to be affecting the job market."

Mark Zandi, the chief economist of Moody's Analytics, said: "The job market remains sturdy in the face of significant fiscal headwinds. Businesses are adding to payrolls more strongly at the start of 2013 with gains across all industries and business sizes. Tax increases and government spending cuts don't appear to be affecting the job market."

The jobs figures and better than expected figures from the service sector helped drive up US stock markets this week. On Tuesday, the Dow Jones industrial average passed levels unseen since before the financial crisis.

In the UK, the stock market shrugged off poor construction figures to reach 6,483, up 44 points. The Office for National Statistics said output fell by 6.3% month on month having fallen by 16.3% in December from November. Worryingly for the chancellor, George Osborne, the figures revealed a sharp fall in infrastructure and civil engineering projects.

Alan Clarke, chief UK economist at Scotia Bank, warned that a triple dip recession was back on the cards without a major boost from other areas of the economy.

The German Dax and French Cac also nudged ahead as large firms, like their UK counterparts, looked ahead to better exports on the back of better news from the US. The US remains the world's largest economy and an important market for European goods.

Even the Italian stock market bounced after the non-farm payroll results, shaking off a credit downgrade that kept the country a few notches above junk status.

Fitch, which downgraded Italy's bond rating to BBB+, from A- with a negative outlook, said: "The increased political uncertainty and non-conducive backdrop for further structural reform measures constitute a further adverse shock to the real economy amidst the deep recession."

The agency expects Italy's output will shrink by 1.8% this year, as Europe's fourth-largest economy struggles in the throes of deepening recession.

Wednesday, February 27, 2013

EUROPE - The twin policy regimes in East and West stoked the credit bubble, and this in turn disguised what has happening to trade flows. These flows were disguised yet further after 2008 by QE and fiscal buffers, but the hard reality beneath may soon be exposed as these are props are knocked away.

EUROPE - The twin policy regimes in East and West stoked the credit bubble, and this in turn disguised what has happening to trade flows. These flows were disguised yet further after 2008 by QE and fiscal buffers, but the hard reality beneath may soon be exposed as these are props are knocked away.

"In a world of deficient demand and excess savings, every country will try to acquire a greater share of global demand by exporting savings," he writes. The "winners" in this will be the deficit states. The "losers" will be the surplus states who cannot retaliate. The lesson of the 1930s is that the creditors are powerless. Prof Pettis argues that China and Germany risk a nasty surprise. America's shale revolution and manufacturing revival may be enough to head off a US-China clash just in time. But Europe has no recovery strategy beyond demand compression. It is a formula for youth job wastage, a demented policy when youth a scarce resource. The region is doomed to decline until the boil of monetary union is lanced. Some will take the Mishkin paper as an admission that QE was a misguided venture. That would be a false conclusion. The West faced a 1931 moment in late 2008. The first round of QE forestalled financial collapse. The second and third rounds of QE have had a diminishing potency, while the risks have risen. It is a shifting calculus. The four years of QE have given us a contained depression and prevented the global strategic order from unravelling. That is not a bad outcome, but the time gained has largely been wasted because few wish to face the awful truth that globalisation itself -- in its current deformed structure -- is the root cause of the whole disaster. ...It will be harder from now on if central banks conclude that their arsenal is spent. We can only pray that their help will not be needed.

Tuesday, February 26, 2013

ECB's purchase of Club Med bond amounts to "monetisation" of public debt in

countries shut out of global markets, whatever the claims of Mario Draghi.

"We see at least a risk that the eurozone is on a path to become more like

Argentina (which of course is why German central bankers are most concerned).

The provinces overspend and are always bailed out by the central government. The

result is a permanent fiscal imbalance for the central government, which then

results in monetization of the debt by the central bank and high inflation," it

said. In America, the Fed would face huge pressure to hold onto its bonds rather

than crystalize losses as yields rise -- in other words, to recoil from

unwinding QE at the proper moment. The authors argue that it would be tantamount

to throwing in the towel on inflation, the start of debt monetisation, or

"fiscal dominance". Markets would be merciless. Bond vigilantes would soon price

in a very different world. Investors have of course been fretting about this for some time. Scott Minerd

from Guggenheim Partners thinks the Fed is already trapped and may have to talk

up gold to $10,000 an ounce to ensure that its own bullion reserves cover

mounting liabilities. What is new is that these worries are surfacing openly in Fed circles. The

Mishkin paper almost certainly reflects a strand of thinking at Constitution

Avenue, so there may be more than meets the eye in last week's Fed minutes,

which rattled bourses across the world with hints of early exit from QE. Mr Bernanke is not going to snatch the punch bowl away just as the US embarks

on fiscal tightening this year of 2pc of GDP, one of the most draconian budget

squeezes in the last century. But he may have concluded that the Fed is sailing

too close to the wind, and must take defensive action soon. Monetarists say this is a specious debate -- arguing that the losses on the

Fed balance sheet are an accounting irrelevancy -- but Bernanke is not a

monetarist. What matters is what he thinks.

ECB's purchase of Club Med bond amounts to "monetisation" of public debt in

countries shut out of global markets, whatever the claims of Mario Draghi.

"We see at least a risk that the eurozone is on a path to become more like

Argentina (which of course is why German central bankers are most concerned).

The provinces overspend and are always bailed out by the central government. The

result is a permanent fiscal imbalance for the central government, which then

results in monetization of the debt by the central bank and high inflation," it

said. In America, the Fed would face huge pressure to hold onto its bonds rather

than crystalize losses as yields rise -- in other words, to recoil from

unwinding QE at the proper moment. The authors argue that it would be tantamount

to throwing in the towel on inflation, the start of debt monetisation, or

"fiscal dominance". Markets would be merciless. Bond vigilantes would soon price

in a very different world. Investors have of course been fretting about this for some time. Scott Minerd

from Guggenheim Partners thinks the Fed is already trapped and may have to talk

up gold to $10,000 an ounce to ensure that its own bullion reserves cover

mounting liabilities. What is new is that these worries are surfacing openly in Fed circles. The

Mishkin paper almost certainly reflects a strand of thinking at Constitution

Avenue, so there may be more than meets the eye in last week's Fed minutes,

which rattled bourses across the world with hints of early exit from QE. Mr Bernanke is not going to snatch the punch bowl away just as the US embarks

on fiscal tightening this year of 2pc of GDP, one of the most draconian budget

squeezes in the last century. But he may have concluded that the Fed is sailing

too close to the wind, and must take defensive action soon. Monetarists say this is a specious debate -- arguing that the losses on the

Fed balance sheet are an accounting irrelevancy -- but Bernanke is not a

monetarist. What matters is what he thinks.

If this is where the Fed is heading, the world is at a critical juncture. The

US economy has not yet reached "escape velocity", and in fact shrank in the 4th

quarter of 2012. Brussels has slashed its eurozone forecast, expecting a second

year of outright contraction in 2013. The triple "puts" of the last eight months -- Bernanke's QE3, Mario Draghi's

Club Med bond rescue, and Beijing's credit blitz -- have done wonders for asset

markets but have not yet ignited a healthy cycle of world growth. Nor can they

easily do do since the East-West trade imbalances that caused the 2008-2009

crisis remain in place.

We know from a body of scholarship that fiscal belt-tightening in countries

with a debt above 80pc to 90pc of GDP is painful and typically self-defeating

unless offset by loose money. The evidence is before our eyes in Greece,

Portugal, and Spain. Tight money has led to self-feeding downward spirals. If

bondyields are higher thannominal GDP growth, the compound effects are deadly.

America may soon get a first taste of this, carrying out the epic fiscal

squeeze needed to bring its debt trajectory back under control with less and

less Fed help. Gross public debt will hit 107pc of GDP by next year, and higher

if the recovery falters as pessimists fear. With the fiscal and monetary shock absorbers exhausted -- or deemed to be --

the only recourse left is to claw back stimulus from foreigners, and that may be

the next chapter of the global crisis as the Long Slump drags on.

Professor Michael Pettis from Beijing University argues in a new book -- "The

Great Rebalancing: Trade, Conflict, and the Perillous Road Ahead" - that the

global trauma of the last five years is a trade conflict masquerading as a debt

crisis.

There is too much industrial plant in the world, and too little demand to

soak up supply, like the 1930s. China is distorting the global system by running

investment near 50pc of GDP, and compressing consumption to 35pc. Nothing like

this has been seen before in modern times. This has nothing to do with the "Confucian" work ethic or a penchant for

stashing away money. Fifty years ago the stereotype was the other way round.

Confucians were seen as feckless. In fact, Chinese families never get the money

in the first place. The exorbitant Chinese savings rate is due to a structure of

taxes, covert subsidies, and banking rules. Variants of this are occuring in many of the surplus trade states. Germany is

doing it in a more subtle way within Euroland. The global savings rate is almost

25pc and climbing to fresh records each year. The overstretched deficit states

in the Anglo-sphere and Club Med are retrenching but others are not picking up

enough of the slack. Germany has tightened fiscal policy to achieve a budget

surplus. This is untenable. In the Noughties the $10 trillion reserve accumulation by Asian exporters and

petro-powers flooded the global bond market. At the same time, the West offset

the deflationary effects of the cheap imports by running negative real interest

rates.

Thursday, February 7, 2013

WELL....recovery from what? How the goalposts have been shifted!

“The financial markets are calmer this morning. But there's plenty of chatter about how the eurozone crisis is back -- if indeed it ever went away...”

Or indeed, if there ever really was one!

The analysis in this blog is utterly misleading rubbish, cleaving the British public from any genuine appreciation of what’s going on in the rest of Europe. And it started out so promisingly too. A pity it has descended into some sort of parrochial branch of an Ambrose Evans-Pritchard-style ‘euro-hate’/ Ukip fundamentalist party rag. Last week, the financial press was full of ‘scratch my head’ stories, trying to explain why the stock markets had climbed to such dizzying heights, against all the struggling fundamentals. Could it be all the fake electronic money sloshing around and having an effect? Could it have anything to do with bonus season? The quiet but dramatic drop in Sterling since Christmas was clearly a bit of sly competitive devaluation – market traders can’t drive it down that far that fast without some seriously organized large trades.

Yesterday, this blog told us with front page, headline confidence that ‘the eurozone crisis was back’ – that political instability over Berlusconi and Rajoy had shaken the markets and caused both the FTSE and the Euro to fall.

But today, the markets are not just ‘calm’, both the FTSE and Euro are UP again. So what’s happened now? Have the traders simply forgotten yesterday’s news? Has the “eurozone crisis” gone away again? Have the “worries” slipped from their gnat-brained memories? Or were they just taking big fat profits from recent gains and using “Eurozone worries” as an excuse? (There were plenty of negative Eurozone stories last week, which had absolutely no effect whatsoever on the rising market.)

Could anyone please remind me again, what exactly the “Eurozone Crisis” actually is these days? I mean, what exactly is it that we are supposed to fear? I thought it was originally a fear about Greece or Portugal or Ireland not being able to service their debt and defaulting, thus toppling banks and the financial system like a series of dominos, but since everybody now has a means of printing unlimited new money, that no longer looks likely to happen. So what unspecified event is it exactly that we now have to fear that justifies the claim “the eurozone crisis is back”?

Are France and Spain going to be swallowed by sink-holes? Are the heads of European governments going to turn into Triffids and eat their own electorate? Really, I mean what precisely is the specific nature of “the Eurozone crisis” now?

It seems to me, that the only real threat now, is of compliant junk reporting driving up bond yields to a point at which bond buyers rub their hands with glee.

This is a crisis of Landfill Consumerism, and we’re ALL implicated up to our necks - it's not just a localised problem for the eurozone.

Call a halt to this pro-market, pro-Tory partisan rubbish blog and open up a rolling blog on the WORLD crisis. It might actually prove to be a better way of documenting, blow-by-blow, the changes the world is currently going through. Investigate all aspects…what do the stocks of resources look like? Raw materials, energy, water, etc? Who’s lying to whom and why? How can the environment possibly cope with a ‘return to growth’, given what we now know about the destructive force of our current business models? You know… some independent analysis, which doesn't merely reflect the stories that the financial markets want to tell.

Subscribe to:

Posts (Atom)

Cyprus will no be the model for future EU bailouts

Cyprus will n be the model for future EU bailouts

Cyprus will be the model for future EU bailouts.

EU word games.

Just like all Humpty Dumpty outfits - when they use a word it means whatever they want it to mean.