New archaeological excavations at the ancient port of Corinth have uncovered evidence of large-scale Roman engineering. Named Lechaion, the port was one of a pair that connected the city of ancient Corinth to Mediterranean trade networks. Lechaion is located on the Gulf of Corinth, while Kenchreai is positioned across the narrow Isthmus of Corinth on the Aegean Sea. These two strategic harbours made Corinth a classical period power, but the Romans destroyed the city in 146 BC when conquering Greece. Julius Caesar rebuilt the city and its harbours in 44 BC, ushering in several centuries of prosperity. Recent excavations by the Lechaion Harbour Project have revealed the impressive engineering of the Roman Empire. Caesar’s Corinthian colony developed into one of the most important ports in the eastern Mediterranean. Ships filled Lechaion with international goods and Corinth became so well known for luxury and vice that a Greek proverb stated, “not everyone can afford to go to Corinth.” However, while ancient coins depict a formidable harbour with a large lighthouse, visible remains of Lechaion are scarce. Visitors to the coastline today can see the foundations of two large structures forming the outer harbour, but otherwise the remains are buried under centuries of sediment. The excavations are beginning to reveal the secrets of this largely forgotten port.

New archaeological excavations at the ancient port of Corinth have uncovered evidence of large-scale Roman engineering. Named Lechaion, the port was one of a pair that connected the city of ancient Corinth to Mediterranean trade networks. Lechaion is located on the Gulf of Corinth, while Kenchreai is positioned across the narrow Isthmus of Corinth on the Aegean Sea. These two strategic harbours made Corinth a classical period power, but the Romans destroyed the city in 146 BC when conquering Greece. Julius Caesar rebuilt the city and its harbours in 44 BC, ushering in several centuries of prosperity. Recent excavations by the Lechaion Harbour Project have revealed the impressive engineering of the Roman Empire. Caesar’s Corinthian colony developed into one of the most important ports in the eastern Mediterranean. Ships filled Lechaion with international goods and Corinth became so well known for luxury and vice that a Greek proverb stated, “not everyone can afford to go to Corinth.” However, while ancient coins depict a formidable harbour with a large lighthouse, visible remains of Lechaion are scarce. Visitors to the coastline today can see the foundations of two large structures forming the outer harbour, but otherwise the remains are buried under centuries of sediment. The excavations are beginning to reveal the secrets of this largely forgotten port.

Access Investments-Building Awareness - European Union-ROMANIA

Showing posts with label EUbusiness. Show all posts

Showing posts with label EUbusiness. Show all posts

Friday, December 15, 2017

New archaeological excavations at the ancient port of Corinth have uncovered evidence of large-scale Roman engineering. Named Lechaion, the port was one of a pair that connected the city of ancient Corinth to Mediterranean trade networks. Lechaion is located on the Gulf of Corinth, while Kenchreai is positioned across the narrow Isthmus of Corinth on the Aegean Sea. These two strategic harbours made Corinth a classical period power, but the Romans destroyed the city in 146 BC when conquering Greece. Julius Caesar rebuilt the city and its harbours in 44 BC, ushering in several centuries of prosperity. Recent excavations by the Lechaion Harbour Project have revealed the impressive engineering of the Roman Empire. Caesar’s Corinthian colony developed into one of the most important ports in the eastern Mediterranean. Ships filled Lechaion with international goods and Corinth became so well known for luxury and vice that a Greek proverb stated, “not everyone can afford to go to Corinth.” However, while ancient coins depict a formidable harbour with a large lighthouse, visible remains of Lechaion are scarce. Visitors to the coastline today can see the foundations of two large structures forming the outer harbour, but otherwise the remains are buried under centuries of sediment. The excavations are beginning to reveal the secrets of this largely forgotten port. Wednesday, February 22, 2017

Relatives of the 12 people killed in December when a truck ploughed into a Christmas market in Berlin have expressed their dismay at the negligent way they say they have been treated by German authorities. About 50 people who lost loved ones in the Islamic State-claimed terrorist attack reportedly told a private meeting called by Germany’s outgoing president, Joachim Gauck, and the interior minister, Thomas de Maizière, they felt abandoned at a deeply upsetting time. Relatives said the first official communication they had with authorities was a bill sent to them by the coroner’s office. The letter reportedly included a warning that if the bill was not paid within a certain timeframe, the recipients would face legal action. One relative told Der Tagesspiegel and Die Welt newspapers that when she received the letter she had thought at the very least it would be a letter of condolence from Berlin’s mayor. Those who were certain that their family members were among the dead said they were prevented by security personnel from entering the Kaiser Wilhelm Memorial church on Breitscheidplatz for a religious service held the day after the attack on 19 December. The reason they were given was that high-ranking German politicians – including Gauck – were among the guests. According to the papers, which reported on the four-hour meeting at Gauck’s Bellevue Palace, the president told the relatives he was distressed to hear they had been unable to enter the church and that he had not known about it at the time.

Relatives of the 12 people killed in December when a truck ploughed into a Christmas market in Berlin have expressed their dismay at the negligent way they say they have been treated by German authorities. About 50 people who lost loved ones in the Islamic State-claimed terrorist attack reportedly told a private meeting called by Germany’s outgoing president, Joachim Gauck, and the interior minister, Thomas de Maizière, they felt abandoned at a deeply upsetting time. Relatives said the first official communication they had with authorities was a bill sent to them by the coroner’s office. The letter reportedly included a warning that if the bill was not paid within a certain timeframe, the recipients would face legal action. One relative told Der Tagesspiegel and Die Welt newspapers that when she received the letter she had thought at the very least it would be a letter of condolence from Berlin’s mayor. Those who were certain that their family members were among the dead said they were prevented by security personnel from entering the Kaiser Wilhelm Memorial church on Breitscheidplatz for a religious service held the day after the attack on 19 December. The reason they were given was that high-ranking German politicians – including Gauck – were among the guests. According to the papers, which reported on the four-hour meeting at Gauck’s Bellevue Palace, the president told the relatives he was distressed to hear they had been unable to enter the church and that he had not known about it at the time.Thursday, January 14, 2016

“The markets have drawn comfort” from the Fed, said Mr Lewis after officials at the central bank said they believed economic developments would “warrant only gradual increases in the federal funds rate”. However, Mr Lewis said further rises presented “a major uncertainty” hanging over both the Fed and markets. “All territory is now uncharted”, he argued, as the US central bank attempts to raise rates from historically low levels, while the banking system is flush with cash.

“The markets have drawn comfort” from the Fed, said Mr Lewis after officials at the central bank said they believed economic developments would “warrant only gradual increases in the federal funds rate”. However, Mr Lewis said further rises presented “a major uncertainty” hanging over both the Fed and markets. “All territory is now uncharted”, he argued, as the US central bank attempts to raise rates from historically low levels, while the banking system is flush with cash.

He added: “The Fed and other major central banks have maintained emergency policy-settings for so long that the global economy cannot be presumed to react in standard fashion to a rise in interest rates, however small that might be.” The central bank, led by chairman Janet Yellen, plans to keep increasing rates by quarter-point increments after raising rates by a quarter of a percentage point from their 0pc to 0.25pc range last month. Stephen Lewis, chief economist at ADM ISI, said that Fed policymakers would regard “the mildness of the response to their action as a tribute to their success”. While the main US index, the S&P 500, closed lower in 2015 as a whole – its first annual loss since the financial crisis – economists have not attributed this to the Fed’s move. Annual wage growth is expected to have picked up from 2.3pc to 2.8pc in December, generating inflationary pressures. Central bank watchers will also pay close attention to the minutes of the Fed’s December meeting, being released on Wednesday. These will show how confident policymakers are in returning inflation to target. The Fed has a mandate to promote full employment and to steer inflation towards 2pc. The inflation measure tracked by US policymakers stood at just 0.4pc in the year to November. Analysts at Barclays said that they expected to see “disparate views on the current state of inflation” and they would “be attentive” to how this impacts on “different views on the most likely path of monetary policy in 2016”.

Wednesday, October 28, 2015

The Eurozone has no fire-power to strengthen. QE has failed because they are already mired deep in a Japanese style deflation trap to which there is no easy escape. Draghi's peashooter has allowed them to standstill for a few months and nothing more. The only thing to be done now is to forcibly devalue the currency and drive it through dollar parity as policy. This is what is necessary to re-establish inflation and growth on the continent. This would be European style economics but may be the only way to save the euro. It must be done now though. The alternative is a slow death and definitely lose the euro. My bet is that the Europhiles cannot face up to what they have done and will therefore opt to do nothing. So it will be the slow death then...the Central Banks are in trouble...and relying on Draghi's monthly or quarterly QE payroll. It's as simple as that. Deflation will hit their books hard. Notice the pressure on Banks to impose charges, more now than ever before. As for Deutsche Bank; it's all their satellites that will feel the pinch....something that Merkel has overlooked at her peril....There is no money. Nobody can buy anything so nobody can sell anything so there is no growth and all kinds of social bills still to be paid through more borrowing along with all the previous debt service costs. Reciprocal debt forgiveness: for some nations temporary retreat from an utterly inappropriate €conomic instrument used as a political weapon that has failed on both battlefields: sustainable, as equable as possible, benefit reduction and an opening of the democracy door to all of the peoples with the same voting weight at all levels are the only answers now. But I think the burden is too great and it is too late, especially with the utterly divisive irritant of the imperial court's decrees on immigration to add to the stew....The ECB printing up more trillions of fiat currency to lavish on their .1% cronies in the financial sector "to combat deflation" (and buy up the distressed assets of the increasingly pauperized middle and working classes at fire sale prices) - my, how groundbreaking. Remind me again of the clinical definition of insanity.

Sunday, May 3, 2015

The US recovery suffered a severe setback at the start of the year with the rate of economic expansion far slower than economists had anticipated, according to data released on Wednesday.

US GDP rose by just 0.05pc in the first quarter, well below the 0.2pc expected by analysts and far weaker than the previous quarter's 0.54pc increase. Analysts blamed the strengthening dollar for the poor performance, as the currency's strength hit exports for a fourth consecutive month. The growth data is likely to stay the Federal Reserve's hands in raising interest rates later this year. The FTSE 100 and dollar both lost ground as the data were released. Chris Williamson, chief economist at Markit, said: "A stalling of US economic growth at the start of the year rules out any imminent hiking of interest rates by the Fed. "The slowdown looks temporary, as a rebound from the first quarter weakness is already being signalled by forward-looking survey data, but the sustainability of any upturn is by no means convincing yet." Ahead of the release, analysts at Deutsche Bank said: "The first quarter of the year has been the weakest in recent years, and 2015 is likely to be no exception”. A string of weak first quarter performances has led some economists to question whether the Commerce Department, which releases the figures is "seasonally adjusting" the data correctly. As a result, some believe that the performances in the second to fourth quarters have been overstated. If that proves to be the case again this year, US growth figures should bounce back

Sunday, February 8, 2015

Greece's finance minister spoke to ECB chief Mario Draghi in Frankfurt (Source: Getty)

In return, Mr Varoufakis assured German voters his government would seek to dismantle the "cronyism and corruption" that has held back the country for decades.

"Germans have to understand that it doesn’t mean we’re turning away from the reform path if we give an additional €300 a year to a pensioner living on €300 a month. When we talk about reforms, we should talk about cartels, about rich Greeks who hardly pay any taxes."

The finance minister ruled out any plea for financial aid from Russia, and called on the German Chancellor to put forward a "Merkel Plan" based on the post-war Marshall loans granted by the United States to rehabilitate Germany after the war.

"I believe the EU would benefit if Germany conceived of itself as a hegemon," said Mr Varoufakis. "But a hegemon must shoulder responsibility for others.

"Germany would use its power to unite Europe. That would be a wonderful legacy for Germany’s federal chancellor."

Who owns Greek debt?

(Source: Open Europe)

Wednesday, September 17, 2014

Russia's ruling party is heading to a convincing victory in Crimea's polls, less than six months after annexing the region.

Russia's ruling party is heading to a convincing victory in Crimea's polls, less than six months after annexing the region.

A preliminary count on Monday showed Crimea's regional branch of the United Russia party was leading with 71.04 percent of votes, after 50 percent of the ballots had been counted, Crimea's electoral commission said. The ultra-nationalist Liberal Democratic Party of Russia (LDPR), led by firebrand lawyer Vladimir Zhirinovsky who backs the Kremlin, was running second with just over eight percent of the vote. No other party appeared to have broken the five percent barrier for representation in the Crimean regional parliament, with a turnout of around 52 percent. The residents of the Black Sea peninsula were voting to select politicians for the parliaments of Crimea and Sevastopol, and for local city councillors. In polls for the regional parliament of the city of Sevastopol, United Russia had won 76 percent, while LDPR won 7 percent, with 65 percent of the votes counted.

Russian Prime Minister Dmitry Medvedev, who leads the United Russia, said the vote proved Russia was acting legitimately in Crimea. "All the participants in the electoral campaign in Crimea have proved to us and our neighbours that power in Russia is based on legal procedures," Medvedev said on Monday in remarks released by the government. However critics called foul, saying politics in the region had come to resemble the Soviet political landscape, with the election characterised by favoritism towards Russian President Vladimir Putin's ruling party. "Suddenly, in three months everything became United Russia here," Andrei Brezhnev, head of the Communist Party of Social Justice said. Ukraine condemned the votes as illegitimate in a statement issued by its foreign ministry.

Tuesday, May 6, 2014

The International Monetary Fund (IMF)

has approved a $17.1bn (£10.1bn) bailout for Ukraine to help the country's

beleaguered economy. The loan comes amid heightened military and political tension between Ukraine

and neighbouring Russia.

The International Monetary Fund (IMF)

has approved a $17.1bn (£10.1bn) bailout for Ukraine to help the country's

beleaguered economy. The loan comes amid heightened military and political tension between Ukraine

and neighbouring Russia.

The loan is dependent on strict economic reforms, including raising taxes and

energy prices.

The money will be released over two years, with the first instalment of

$3.2bn available immediately.

The head of the IMF, Christine Lagarde, said the IMF would check regularly to

ensure the Ukrainian government followed through on its commitments.

In March Ukraine put up gas prices by 50% in an effort to secure the

bailout.

The government has also agreed to freeze the minimum wage.

The bailout had to be approved by the IMF's 24-member board, which includes a

Russian representative.

The IMF loan will also unlock further funds worth $15bn from other donors,

including the World Bank, EU, Canada and Japan.

Russian recession

In December last year, Ukraine agreed a $15bn bailout from Russia, but this

was cancelled after protests forced out pro-Russian President Viktor

Yanukovych....

The IMF bailout will also make available $1bn in loan guarantees from the US,

which was recently approved by Congress.

"Today's final approval for the $17bn IMF programme marks a crucial milestone

for Ukraine," said US Treasury Secretary Jacob Lew in a statement.

He added that the bailout will "enable Ukraine to build on the progress

already achieved to overcome deep-seated economic challenges and help the

country return to a path of economic stability and growth".Earlier on Wednesday, an international conference in London ended with a commitment to help Ukraine recover tens of billions of dollars worth of assets which were allegedly stolen by the ousted President Yanukovych and his allies.

The IMF warned that Russia was "experiencing recession" because

of damage caused by the Ukraine crisis.

Tuesday, March 18, 2014

Wednesday, January 8, 2014

The slump in business lending has deepened, it has emerged, further sharpening the contrast with a surging mortgage market.

The slump in business lending has deepened, it has emerged, further sharpening the contrast with a surging mortgage market.

Companies took £4.7bn less in loans in November, the biggest drop in more than two years and nearly five times the recent average monthly decline of £1bn, according to figures from the Bank of England. The slide was due to a fall in lending to large businesses, as loans to small and medium-sized companies actually edged up slightly.

Economists are split over whether the decline is due to weak demand for bank finance or lenders’ reluctance to grant loans to business.

Howard Archer, chief UK economist at IHS, said the data suggested that banks “have yet to become markedly more prepared to lend to businesses amid the improved economic situation and outlook”. But Blerina Uruçi, economist at Barclays, believes businesses are unlikely to be held back by weak bank finance as the corporate sector has amassed a large cash surplus in recent years. Businesses are also increasingly turning to the bond market as a cheaper alternative.

Mark Carney, governor of the Bank of England, has redoubled efforts to boost business lending by making it the sole beneficiary of the Funding for Lending Scheme, which allows lenders to borrow at rock-bottom rates in exchange for providing loans. Previously, the scheme applied to all loans.

Sunday, December 22, 2013

Stupid is what Stupid does ...judge for yourself !

Credit rating agency Standard & Poor's incited the ire of European Union officials on Friday when it snatched away the region's top AAA rating, citing tensions between member states and a deterioration in their overall financial health.

Downgrading the EU to AA+, the agency said the 28 countries' combined creditworthiness had declined – but officials and leaders shot back with an assertion that the region had barely any outstanding debt relative to GDP.

Ireland experienced an exceptionally enormous deficit of 31% of its GDP in 2010, largely due to the cost of rescuing its banks.

Italy, however, has faired surprisingly well. In fact, if you exclude the cost of interest payments on its enormous debts (which the graph does not), the Italian government has consistently run budget surpluses.

EU rules say that countries using the euro are not

allowed to have an annual deficit of more than 3% of GDP, but several countries

have failed to keep to that rule in recent years.

Note that Germany, Italy and France were all among the first countries to

break the Maastricht rule during the last decade, while Spain and the Republic

of Ireland ran surpluses before the 2008 crisis. Since 2008, peripheral economies such as Spain, Greece and Portugal have run

big deficits, because their economies have slumped, generating less tax revenues

and requiring more unemployment benefit payments.Ireland experienced an exceptionally enormous deficit of 31% of its GDP in 2010, largely due to the cost of rescuing its banks.

Italy, however, has faired surprisingly well. In fact, if you exclude the cost of interest payments on its enormous debts (which the graph does not), the Italian government has consistently run budget surpluses.

Tuesday, December 10, 2013

Britain will give an extra £10bn to the European Union because of the weakness of struggling eurozone economies, it has emerged. The British contribution to the EU will rise dramatically from £30bn to £40bn over the next five years, the Office for Budget Responsibility said. It includes a surprise £2.2bn jump in funding to £8.7bn this year. EU contributions are calculated in part according to each state’s national income. The growth forecasts across Europe have been cut as eurozone economies, particularly Greece, France and Italy, struggle under a debt crisis, leaving Britain to make up the shortfall – costing the taxpayer an extra £1bn a year. How much longer are the taxpayers of this once great country going to tolerate the increasing financial support of this failing, tyrannical dictatorship, especially while our own public services are declining?

Britain will give an extra £10bn to the European Union because of the weakness of struggling eurozone economies, it has emerged. The British contribution to the EU will rise dramatically from £30bn to £40bn over the next five years, the Office for Budget Responsibility said. It includes a surprise £2.2bn jump in funding to £8.7bn this year. EU contributions are calculated in part according to each state’s national income. The growth forecasts across Europe have been cut as eurozone economies, particularly Greece, France and Italy, struggle under a debt crisis, leaving Britain to make up the shortfall – costing the taxpayer an extra £1bn a year. How much longer are the taxpayers of this once great country going to tolerate the increasing financial support of this failing, tyrannical dictatorship, especially while our own public services are declining?Are our fools and cretins of politicians, who are mostly in favor of this abomination waiting to be physically removed from Parliament?

The entire lib/lab/con are hell bent on keeping Britain in the EU, so it's time they were all removed from government!...If you take into account, the money Britain will have to spend to "welcome" the people from Bulgaria and Romania heading towards what they think is an Eldorado, it is much more than £10 billions. Thank you very much, anyway, as a French, I rather see them coming in the UK and as you are explained day after day by people living in huge houses in Surrey, with private medical care and with their children privately educated that it is for your benefit, you should call yourselves lucky.... "It includes a surprise £2.2bn jump in funding to £8.7bn this year." This wasn't a surprise, the EU came begging for a bail out, what was surprising, was the little press it received?

This is why we are needed in the EU, to pay for all the little countries they admit, even when their finances don't meet the criteria! From next June, we will be powerless in our decision making, the EU / US FTA is due to be signed then, this deal, gives companies complete control over us, even now, Tobacco giant Philip Morris is suing Australia for billions of dollars in lost profits because the government took action to reduce teenage smoking. Pharmaceutical giant Eli Lilly is suing Canada for $500 million, just because Canada has laws to keep essential drugs affordable and the Nuclear industry is suing the German government. This is all happening in International courts, out of the public eye, via other TTiP deals. Lets get together and stop this one!

The chancellor warned Britain is “too dependent” on weak European markets and must look to the Far East for growth.

The Euro area is forecast to shrink by 0.4 per cent this year and instability in the region is the first threat to Britain’s recovery, Mr Osborne said. He has doubled the export finance capacity to £50bn to support British businesses that want to trade in new markets.

“The Prime Minister’s visit to China this week is the latest step in this Government’s determined plan to increase British exports to the faster growing emerging markets – something our country should have done many years ago,” Mr Osborne said.

Friday, November 22, 2013

The European parliament has backed rules that would give women preference for non-executive posts at companies, after plans for a mandatory quota to get women into top jobs were scrapped.

The European parliament has backed rules that would give women preference for non-executive posts at companies, after plans for a mandatory quota to get women into top jobs were scrapped.

The rules demand that companies give non-executive directorships to women where there is no male candidate who is better qualified, until they reach a target of four in 10 being women.

"The parliament has made the first cracks in the glass ceiling that continues to bar female talent from the top jobs," said EU justice commissioner Viviane Reding, who launched the proposal.

Although the draft law envisages possible fines for firms that ignore selection rules, it has been softened from imposing a quota with a penalty. Nor do the rules help women aiming for top management roles, such as chief executive. They also exempt smaller companies and those that are not listed.

Only about 17% of non-executive board members in the EU's largest companies are women. In Britain, women hold 17.4% percent of directorships, up from 12.5% in 2010; only four CEOs at FTSE 100 companies are women.

If endorsed, the rules will take seven years to come into full force. Countries are now required to sign off on the law but are divided on whether pan-European rules on positive discrimination are necessary.

Britain and Germany have argued against mandatory quotas.

Men dominate boardrooms in the region, and many women who have risen through company ranks resent quotas because they can be seen as suggesting that women have not been promoted on merit.

Only Norway, which is not a member of the bloc, has enforced a 40% quota since 2009, although critics say this has been achieved in part thanks to a small number of women holding non-executive positions in multiple companies.

"It is essential for listed companies to evolve so as to include highly skilled women in their decision-making processes," said Rodi Kratsa-Tsagaropoulou, a member of the parliament who is playing a central role in shaping the law.

Sunday, November 17, 2013

Hopefully, in their blind obedience to Merkel and co, the amazingly stupid and corrupt EU Commission will have gone yet another step too far. IF You are Italian or Spanish and you read the headline in your local paper that the EU wants to make you poorer and take more power to themselves from your Government...I think ropes and lamposts are in order for the EU Commissioners if they go much further.

Germany's status as Europe’s industrial powerhouse could be damaging the single-currency bloc, the European Commission has said, as it launched a probe into whether the country’s large trade surplus was hindering Europe’s recovery. Europe’s biggest economy was one of three countries singled out for an “in-depth review” by the EC’s Alert Mechanism Report on Wednesday. The Commission said Germany’s large current account surplus, which accounts for most of the eurozone’s positive balance, “may put pressure on the euro to appreciate vis-à-vis other currencies. “In case such pressures materialise, this would make it more difficult for the peripheral countries to recover competitiveness through internal depreciation,” it said. However, Brussels insisted it was not criticising Germany’s economic success. “The issue is whether Germany ... could do more to help rebalance the European economy,” said Jose Manuel Barroso, the president of the EC. Olli Rehn, commissioner for economic and monetary affairs, added: “Let’s be clear, we are not criticising Germany’s external economic competitiveness or its success in global markets, in fact that is what we want from all EU member states,” However, Mr Rehn said Germany’s “persistent high surplus also means that Germans are persistently investing a large part of their savings abroad. The question is whether this is efficient, even from the German perspective.” The EC also fired a warning shot at Britain, and said rising house prices would restrain households’ ability to cut debt. The Commission highlighted Britain’s unbalanced recovery. According to Eurostat, Britain’s share of world exports declined by 19pc between 2007 and 2012. The EC said levels of Government debt in UK remained a concern, while the “ongoing balance sheet repair of the financial sector and the persistent scarcity of credit for smaller firms may continue to hold back economic growth.” EC data last week predicted Britain’s commercial deficit will be the highest in a quarter century next year, at 4.4pc of GDP. Meanwhile, low-tax, banking-rich Luxembourg, and Croatia, which accepted a bailout this year, were also added to the EC’s watch list.

Friday, November 8, 2013

The European Union wasted almost £6 billion last year on fraudulent, illegal or ineligible spending projects, official auditors have found.

The European Union wasted almost £6 billion last year on fraudulent, illegal or ineligible spending projects, official auditors have found.

At a time of unprecedented European-wide austerity, the EU mis-spent almost 5 per cent of its budget in 2012 on projects that should never have received any of its money.

This so-called ‘error rate’ in Brussels spending was up from 3.9 per cent the previous year, according to the auditors. It meant that for the 19th year in a row, they refused to give the EU’s accounts a clean bill of health.

EU bureaucrats were accused of “shambolic” mismanagement yesterday in the wake of the report, with Conservative MEPs suggesting it appeared as though Brussels simply had a licence to Carry on Squandering’.

The European Court Auditors (ECA) found that 4.8 per cent of the EU’s £117 billion budget in 2012 - £5.7 billion - was spent in “error”, on projects that were either tainted by fraud or ineligible for grants under Brussels’ rules. This meant British taxpayers saw up to £832 million of their contributions to the EU wasted at a time of deep public spending cuts domestically. The EU spending watchdog found that supervision and control of Brussels spending was only “partially effective in ensuring the legality and regularity of payments underlying the accounts”.

“All policy groups covering operational expenditure are materially affected by error,” the auditors concluded.

“For these reasons it is the ECA’s opinion that payments underlying the accounts are materially affected by error.”

A British Government spokesman yesterday described the findings as “unacceptable and undermining the credibility of EU spending”.

“When countries across Europe are taking difficult decisions to tackle their deficits, Europe’s taxpayers need to have confidence that every effort is being made to improve the way EU spending is managed,” she said.

Included among the “errors” discovered by the auditors was a Polish landowner paid almost £80,000 a year to maintain 350 acres of grassland to help preserve uncut grassland for the protection of endangered bird species. In fact, the farmer had only met the agreed funding requirements for 14 per cent of the land and the payments.

“Similar cases of non-compliance with agri-environment requirements were detected in the Czech Republic, Germany , Greece, France and the United Kingdom,” found the auditors.

The EU’s regional policy spending had an error rate of 6.8 per cent, or £2.4 billion, of the £34 billionn spent in 2012. Most ineligible funding followed a failure to follow EU laws on public procurement and issuing of contracts.

The error rate in “external relations, aid and enlargement” spending overseen by Baroness Ashton, the EU foreign minister, totalled 3.3 per cent, or £169 million of £5 billion in spending.

In one case, the European Commission paid £14 million for a programme to support female teachers in rural Bangladesh but over half the money was given with “no documentation”.

Philip Bradbourn MEP, the Conservative spokesman on EU budgetary control, described the latest audit as “another year, another story of lax monitoring and shambolic control”.

“If you found misappropriation and misspending on this scale in a commercial business — or in a properly-accountable public administration — there would be sackings all round. In Brussels, it’s ’Carry on Squandering’,” he said.

Vitor Caldeira, the president of the EU auditors, warned that poor financial planning by the European Commission for “will put added pressure on EU cash flows and may increase the risk of error over the next few years”.

“Europe’s citizens have a right to know what their money is being spent on and whether it is being used properly,” he said.

Meanwhile, EU funds worth £418 million intended to help rebuild the Italian city of L’Aquila and the Abruzzo region after an 2009 earthquake have been mired in suspected corruption, a separate European Parliament report has found.

Serious allegations have surfaced that part of the money spent on building new accommodation for the earthquake’s victims was paid to companies with “direct or indirect ties” to organised crime because it was paid in breach of public procurement rules.

Monday, October 28, 2013

FRANKFURT--The European Central Bank will force the euro zone's largest banks

to set aside 8% of their risk-adjusted assets as a capital buffer, which will

form one plank of the ECB's assessment of bank balance sheets next year,

according to a person familiar with the matter. Euro-zone banks, which will be supervised by the ECB starting at the end of

next year, will be required to hold a 7% capital buffer. The region's most

significant banks will have to hold an additional percentage point, the person

said. The buffers protect banks against losses they may take on loans and other

assets. An ECB spokesman declined to comment.

FRANKFURT--The European Central Bank will force the euro zone's largest banks

to set aside 8% of their risk-adjusted assets as a capital buffer, which will

form one plank of the ECB's assessment of bank balance sheets next year,

according to a person familiar with the matter. Euro-zone banks, which will be supervised by the ECB starting at the end of

next year, will be required to hold a 7% capital buffer. The region's most

significant banks will have to hold an additional percentage point, the person

said. The buffers protect banks against losses they may take on loans and other

assets. An ECB spokesman declined to comment.

The target of 7% is in line with what a bank has to achieve under the new

"Basel III" rules on capital in order to pay its dividends and bonuses without

restrictions. However, it's lower than the 9% required by the capital exercise

that the European Banking Authority carried out over 2011-2012. Theoretically,

the new Basel standards don't come into force until 2018, but pressure from both

regulators and financial markets has led most banks to report under the new

standards already. The one percentage point surcharge for 'significant' banks echoes the

Financial Stability Board's intention to impose a capital surcharge of up to 3.5

percentage points for Systemically Important Financial Institutions--also known

as banks that are 'too big to fail.' The FSB will phase in these surcharges between 2016-2019. According to its

latest assessments, Deutsche Bank AG (DBK.XE) would be liable to a surcharge of

2.5 percentage points, with a dozen other EU banks being subject to surcharges

of between one and two percentage points. However, it isn't clear how the ECB

will define its list of significant banks.

The ECB will release additional details on how it will handle its asset

quality review at a press conference Wednesday. Europe's central bank will

conduct the review in the first half of next year, before it takes on the role

of bank supervisor. Currently, banks across the 17-member currency bloc are

overseen by national regulators. The review is seen by most analysts as a critical part of efforts by European

officials to address capital needs of banks, particularly in southern Europe,

and to spur new lending to the private sector.

Tuesday, October 22, 2013

Several hundreds of people were protesting in the village of Silistea-Pungesti in Eastern Romania on Wednesday against plans by US company Chevron to start operating the first shale gas exploration drill in the county of Vaslui, news agency Agerpres reports.

Several hundreds of people were protesting in the village of Silistea-Pungesti in Eastern Romania on Wednesday against plans by US company Chevron to start operating the first shale gas exploration drill in the county of Vaslui, news agency Agerpres reports.

Protesters - some of whom have come from the Barlad, Iasi and other cities in the region of Moldova, Eastern Romania, some of whom are locals from Pungesti - installed tents on the field where Chevron machines are to be deployed. They remained there over night to protest today and said they would not leave the perimeter and would not allow representatives of the US company to come to the area.

On Wednesday afternoon, some 500 people were taking part in the protest. Some locals forced a line of intervention police deployed in the area and managed to reach the perimeter they were not allowed in. Vaslui county prefect Radu Renga warned that laws must be complied it and that gendarmes have to intervene when public order and traffic on public roads are affected.

The first exploration drill is to be deployed in the close vicinity of the village of Pungesti.

Chevron Romania holds another three certificates for the county of Vaslui to start explorations in order to identify possible shale gas reserves.

Monday, October 7, 2013

It changes by the hour ....what a circus !!! lies and deceit and that's all !!

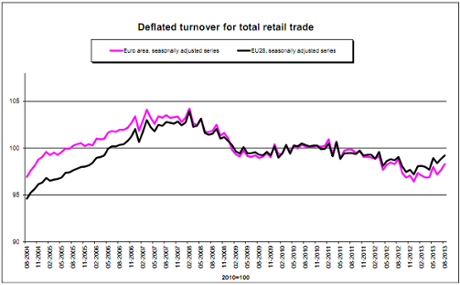

Good news for the European economy: retail sales were much stronger than expected in August.

Good news for the European economy: retail sales were much stronger than expected in August.

Eurostat reported that retail sales volumes rose by 0.7% in the euro area, and 0.4% across the wider European Union in August. July's data was also revised higher, showing consumers weren't as cautious about spending as first thought.

Eurostat's data shows that non-food shopping was strong, rising by 0.6% in the eurozone. That covers items such as computers, clothing and medical products.

The data also showed an increase in fuel purchases, suggesting a rise in motor journeys. Spending on "automotive fuel in specialized stores" (that's petrol stations to you and me) was up by 0.9% across euro members.

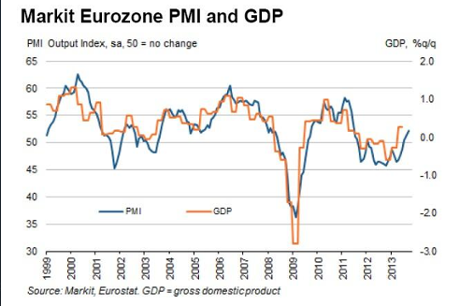

The eurozone recovery is gathering pace, with its private sector firms reporting the biggest leap in activity since June 2011 last month.

Data firm Markit's monthly surveys of companies across the single currency showed a solid rise in activity.

New business has picked up, and the rate of job cuts may finally be slowing to a halt.

Markit's monthly survey of activity came in at 52.2, up from August's 51.5. Both service sector firms and manufacturers said conditions were better.

Ireland: 55.7 2-month low

Germany: 53.2 2-month low

Italy: 52.8 29-month high

France: 50.5 20-month high

Spain: 49.6 2-month low

Germany: 53.2 2-month low

Italy: 52.8 29-month high

France: 50.5 20-month high

Spain: 49.6 2-month low

The news comes hours after China's service sector output hit a 6-month high.

Chris Williamson, chief economist at Markit, said the eurozone data showed Europe's recovery on track, despite Spain's private firms faltering after a better August.

Thursday, October 3, 2013

The truth about Merkel's 4th. Reich

It's becoming clear how hard is going to be for Frau Merkel to form a new government. The SPD wants the Finance Ministry and will ballot its members on any deal. In the end, though, they're likely to reach an agreement, say media commentators.

The election may have been held eight days ago, but Germany is no closer to forming a government. It could take until December or January, the general secretary of the opposition Social Democrats (SPD), Andrea Nahles, warned on Monday. The SPD, in a canny move to drive up its price for joining a coalition and to secure grass-roots support for a deal, decided at a party conference on Friday that it will ballot its 470,000 members on any agreement. That means they can say in talks, "we can't give in on that point because our members won't back it. That's bad news for Chancellor Angela Merkel, because it will make the talks to form a so-called grand coalition of the two main parties all the more difficult. As if that weren't enough, Bavarian governor Horst Seehofer, an important conservative ally of hers, on Sunday narrowed her negotiating position with some undiplomatic rhetoric before preliminary talks had even begun.

Sunday, September 29, 2013

Subscribe to:

Posts (Atom)