“We must leave the austerity cage,” he told leaders of his Democrat Party

(Pd), responding to Italy’s electoral earthquake by tearing up his pre-election

programme. “A change of course is absolutely necessary given that five years of

austerity and attacks on workers have pushed up public debt levels across

Europe,” he said.

“We must leave the austerity cage,” he told leaders of his Democrat Party

(Pd), responding to Italy’s electoral earthquake by tearing up his pre-election

programme. “A change of course is absolutely necessary given that five years of

austerity and attacks on workers have pushed up public debt levels across

Europe,” he said.

“The vicious circle between belt-tightening and recession is putting

representative government at risk and making it impossible to govern. The

immediate emergency is the real economy and joblessness,” he said. The pledge puts Mr Bersani on a collision course with the ECB, which is

constrained from helping to shore up the Italian bond market unless Rome

complies with Europe’s austerity agenda. “Italian voters may have effectively voted away the ECB safety net,” said

Christian Schulz from Berenberg Bank. The central bank cannot activate its bond

purchase programme (OMT) unless Italy requests a rescue from the EMU bail-out

fund, and that in turn requires a vote in Germany’s Bundestag.

“The ECB cannot – and will not want to – do anything to help Italy after the

inconclusive election result, even if borrowing costs spiral out of control,” he

said.

Mr Bersani’s Democrats (Pd) and its allies control the lower house but failed

to win the senate. He is hoping for tacit support on a law-by-law basis from the

Five Star Movement of comedian Beppe Grillo. Mr Grillo has responded with a volley of anathemas, calling Mr Bersani a

relic from a defunct political order that must be swept away by civic

revolution. Yet many of his 163 senators and deputies say the movement should

seek common ground with the Pd.

Mr Bersani said Italy should mobilize its EU voting weight to push for an

EU-wide change of course. He has natural allies in Paris.

French finance minister Pierre Moscovici warned EMU colleagues on Monday that

current policies “risk a loss of social and political confidence across Europe.

We must not pile austerity on top of recession”. Mr Moscovici said France would need an extra year to meet its deficit target

of 3pc of GDP and called for action to tackle the root of the crisis with an

EMU-wide growth strategy.

French officials are deeply alarmed by the relentless upward rise in France’s

unemployment rate to 10.6pc, or 26.9pc for youth. President Francois Hollande’s

popularity ratings have crashed from 55pc to 30pc since his election in May, the

fastest decline ever recorded for a French leader.

Italy, France, and Spain toyed with a Latin bloc alliance last year to

confront Germany over EMU’s contractionary policy mix, but the initiative faded.

Mr Hollande pulled back from a showdown with Berlin and ultimately pushed

through further fiscal cuts and reforms, while Italy’s Mario Monti was never

willing to jeopardise the European Project that he served for ten years as a

commissioner.

Critics says Mr Monti, whose Civic Choice list won just 10pc of the vote,

went native in Brussels long ago and has been slow to understand the deeper

political crisis unfolding in Italy.

The outgoing premier gave them fresh ammunition today, saying that it would

be better to hold fresh elections than to see an anti-EU government to take

power.

It is unclear whether a second vote would achieve what he intends. The latest

snap polls show that Mr Grillo’s support is still rising, jumping from 25pc to

28pc.

Ominously, nostalgia for Fascist leader Benito Mussolini has started to

emerge as the post-War order crumbles. Two key figures have praised elements of

Fascist rule over the last two days.

A leader of the Five Star Movement professed “fascination” with the Fascist

sense of the Italian state and the family, while the deputy state secretary of

the economy said Mussolini “governed well until 1935.” (source telegraph)

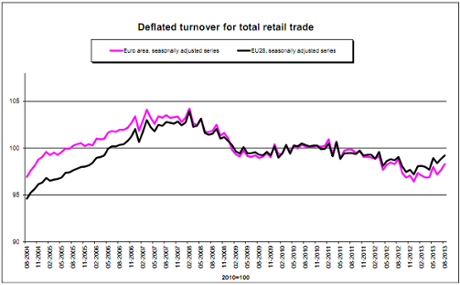

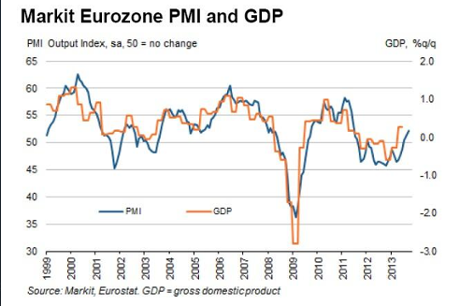

Good news for the European economy: retail sales were much stronger than expected in August.

Good news for the European economy: retail sales were much stronger than expected in August.