Access Investments-Building Awareness - European Union-ROMANIA

Showing posts with label banks. Show all posts

Showing posts with label banks. Show all posts

Tuesday, January 19, 2016

Thursday, June 18, 2015

Finland and Russia. Well

Finland is the only EU member nation to border Russia and not be a NATO member.

I suspect they are wary of Russia but have a greater understanding of Russia's

somewhat justified paranoia and anger with broken ' influence space' NATO

invasions since the 1990's. They seek the old USSR relationship probably which

worked well for Finland. Your last sentence captures this. BTW by many polls

the most pro-EU Nordic - not members yet (and they were in the list with

Denmark, UK and Ireland in the 1960's - is Norway. Following April's elections, Juha Sipila, the prime minister, Timo Soini, the

eurosceptic foreign minister and Alexander Stubb, the finance minister, have

pledged to create more jobs, to get the economy moving and avoid a "lost decade"

from a lack of reforms. Finland is out on its own compared to the other Nordic countries in joining

the Euro. Norway isn't even in the EU, Sweden has done well keeping the Krona

and Denmark has kept their Krona but ties it to the Euro, a tie that could

easily be broken if the proverbial hits the fan. Finland is looking rather

isolated. Of course the Baltic states are in the Euro but they have all paid a

heavy price for membership. Would I be right in thinking that Finland is being hurt by Russian

retaliatory sanctions rather more than other countries? Whilst they must have an

historical healthy fear of Russia, I would imagine they are far more scared

about the West restarting the Cold war in extreme earnest because of western

interference in the internal affairs of Ukraine.

Finland and Russia. Well

Finland is the only EU member nation to border Russia and not be a NATO member.

I suspect they are wary of Russia but have a greater understanding of Russia's

somewhat justified paranoia and anger with broken ' influence space' NATO

invasions since the 1990's. They seek the old USSR relationship probably which

worked well for Finland. Your last sentence captures this. BTW by many polls

the most pro-EU Nordic - not members yet (and they were in the list with

Denmark, UK and Ireland in the 1960's - is Norway. Following April's elections, Juha Sipila, the prime minister, Timo Soini, the

eurosceptic foreign minister and Alexander Stubb, the finance minister, have

pledged to create more jobs, to get the economy moving and avoid a "lost decade"

from a lack of reforms. Finland is out on its own compared to the other Nordic countries in joining

the Euro. Norway isn't even in the EU, Sweden has done well keeping the Krona

and Denmark has kept their Krona but ties it to the Euro, a tie that could

easily be broken if the proverbial hits the fan. Finland is looking rather

isolated. Of course the Baltic states are in the Euro but they have all paid a

heavy price for membership. Would I be right in thinking that Finland is being hurt by Russian

retaliatory sanctions rather more than other countries? Whilst they must have an

historical healthy fear of Russia, I would imagine they are far more scared

about the West restarting the Cold war in extreme earnest because of western

interference in the internal affairs of Ukraine.Friday, December 13, 2013

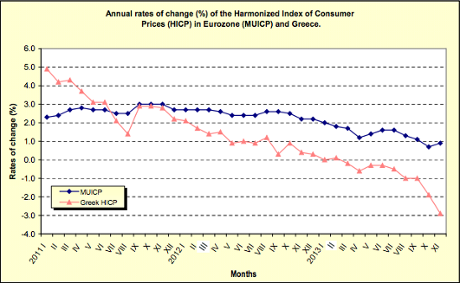

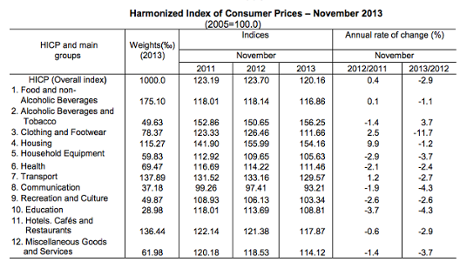

Greek deflation rate hits new high

Greece has lurched further into deflation, with prices tumbling at the fastest rate recorded as the country's long economic slump continues.

The Greek consumer prices index shrank by 2.9% in November, showing deflation accelerated after October's reading of minus 2.0%.

Prices in Greece have been falling steadily over the last three years, hitting deflation in April for the first time since records began in the 1960s.

This graph tracks Greek CPI (red) against eurozone inflation (blue):

Today's data shows that some retailers have slashed prices drastically, having seen demand slide among customers buffeted by austerity cutbacks and record unemployment.

Clothing and textile prices tumbled by over 11%, according to national statistics body ELSTAT. Household equipment costs were down 3.7% year-on-year, as this chart shows:

Greece's austerity programme has forced wages and pensions down in an attempt to boost competitiveness -- so deflation has not come as a surprise. It could even be taken as a sign that the Troika's plan is having its intended effect.

The damage wrecked on the wider Greek economy rather undermines the argument that deflation's a good thing, though, especially as Athens isn't able to inflate away some of its national debt.

We've also heard confirmation this morning that the Greek economy shank by 3% on a year-on-year basis in Q3, which confirms that the five-year recession is easing.

Sunday, November 17, 2013

Hopefully, in their blind obedience to Merkel and co, the amazingly stupid and corrupt EU Commission will have gone yet another step too far. IF You are Italian or Spanish and you read the headline in your local paper that the EU wants to make you poorer and take more power to themselves from your Government...I think ropes and lamposts are in order for the EU Commissioners if they go much further.

Germany's status as Europe’s industrial powerhouse could be damaging the single-currency bloc, the European Commission has said, as it launched a probe into whether the country’s large trade surplus was hindering Europe’s recovery. Europe’s biggest economy was one of three countries singled out for an “in-depth review” by the EC’s Alert Mechanism Report on Wednesday. The Commission said Germany’s large current account surplus, which accounts for most of the eurozone’s positive balance, “may put pressure on the euro to appreciate vis-à-vis other currencies. “In case such pressures materialise, this would make it more difficult for the peripheral countries to recover competitiveness through internal depreciation,” it said. However, Brussels insisted it was not criticising Germany’s economic success. “The issue is whether Germany ... could do more to help rebalance the European economy,” said Jose Manuel Barroso, the president of the EC. Olli Rehn, commissioner for economic and monetary affairs, added: “Let’s be clear, we are not criticising Germany’s external economic competitiveness or its success in global markets, in fact that is what we want from all EU member states,” However, Mr Rehn said Germany’s “persistent high surplus also means that Germans are persistently investing a large part of their savings abroad. The question is whether this is efficient, even from the German perspective.” The EC also fired a warning shot at Britain, and said rising house prices would restrain households’ ability to cut debt. The Commission highlighted Britain’s unbalanced recovery. According to Eurostat, Britain’s share of world exports declined by 19pc between 2007 and 2012. The EC said levels of Government debt in UK remained a concern, while the “ongoing balance sheet repair of the financial sector and the persistent scarcity of credit for smaller firms may continue to hold back economic growth.” EC data last week predicted Britain’s commercial deficit will be the highest in a quarter century next year, at 4.4pc of GDP. Meanwhile, low-tax, banking-rich Luxembourg, and Croatia, which accepted a bailout this year, were also added to the EC’s watch list.

Sunday, October 27, 2013

Central bank governors and senior regulators are set to ordain that banks must have a minimum core tier one capital ratio, including a new so-called "buffer" to protect against extreme economic conditions, of 7%, I can reveal.

Central bank governors and senior regulators are set to ordain that banks must have a minimum core tier one capital ratio, including a new so-called "buffer" to protect against extreme economic conditions, of 7%, I can reveal.

This is considerably lower than was wanted by the "hawks", the US, UK and Switzerland. They wanted a core tier one capital ratio of 8 to 9% including buffer, which is what British banks currently have to maintain. In fact most British banks currently have a core tier one ratio of around 10%.

But the new 7% minimum has been agreed in the face of stiff resistance from a number of countries, led by Germany, many of whose banks typically have much lower stocks of core capital in the form of equity and retained earnings - and will have great difficulty meeting the new standard.

This new international minimum was negotiated by regulatory and central banking officials in a meeting of the Basel Committee on Banking Supervision earlier this week. It is expected to be approved by the governors and senior regulators when they meet in Basle on Sunday. It will then be ratified in a final, supposedly irrevocable way by the heads of the G20 governments, at their summit in November. The 7% minimum represents a dramatic increase on the current minimum of 2%. That 2% minimum is widely seen as far too low: banks' low levels of capital relative to their assets was a major contributor to the severity of the 2008 banking crisis, as investors lost confidence in their ability to survive losses.

As they approached collapse, the capital ratios of Northern Rock and Royal Bank of Scotland fell to dangerously low levels - which is why Northern Rock was nationalized and RBS was semi-nationalized.

The point of capital is to absorb losses when loans and investments turn bad.

Although this new 7% minimum ratio of core capital (in the form of equity and retained earnings) to assets (loans and investments) as measured on a risk-weighted basis represents a significant increase, some will argue that the ratio is still too low.

One reason for this is that the absolute minimum capital ratio, without buffer, will be around 4%, or double the previous minimum.

Under the new system, if a bank's capital ratio falls below 7% or would fall below 7% when the bank is tested for financial stresses, the bank will be forced by regulators to raise new capital. And if the ratio falls below 4%, the bank will be put into "resolution" - which means that it will be taken over by regulators and wound up.

It means that banks' core capital ratios must always be above 7% in normal economic and financial conditions. But regulators would tolerate those ratios falling below 7% for short periods during economic downturns.

A senior regulator has told me that many of the biggest banks - those "too-big-to-fail" banks whose collapse would cause ruptures to the financial system - will in practice be forced to hold more than the 7% minimum.

"There will be some kind of add-on for systemically important banks," he said. So the likes of Barclays, JP Morgan, Royal Bank of Scotland, UBS and so on will in practice have to maintain core capital ratios greater than 7%.

The major concern of banks about the imposition of the higher capital ratios is that it will constrain their ability to lend in the transition period, as they build up stocks of capital - and that could undermine the global economic recovery.

The point is that there are two ways for banks to raise capital ratios: they can persuade investors to buy new shares; or they can shrink their balance sheets relative to their existing stock of capital by lending and investing less.

Because of the threat to economic growth of rapid implementation of the new capital ratios, the regulators and central bank governors are expected to give banks several years to meet the new standards.

The Basel Committee on Banking Supervision softened some of its proposed capital and liquidity rules while introducing new restrictions on how much lenders can borrow in order to rein in their risk-taking.

The panel agreed yesterday to allow certain assets, including minority stakes in other financial firms, to count as capital, according to a statement. The committee set a leverage ratio to apply to banks globally for the first time, which could become binding by 2018, pending further adjustments to the method of calculating banks’ assets.

“Even after all the compromises, the banks aren’t off the hook from tighter capital and liquidity rules,” said Frederick Cannon, chief equity strategist at New York-based Keefe, Bruyette & Woods.

France and Germany have led efforts to weaken rules proposed by the committee in December, concerned that their banks and economies won’t be able to bear the burden of tougher capital requirements until a recovery takes hold, according to bankers, regulators and lobbyists involved in the talks. The U.S., Switzerland and the U.K. have resisted those efforts. The announcement reflects the give and take between the two sides, said Barbara Matthews, managing director of BCM International Regulatory Analytics LLC in Washington.

German Concerns

Germany hasn’t signed yesterday’s preliminary agreement, said Sabine Reimer, a spokeswoman for BaFin, the country’s financial regulator.

“One country still has concerns and has reserved its position until the decisions on calibration and phase-in arrangements are finalized in September,” the committee said in a footnote to its statement.

Sumitomo Mitsui Financial Group Inc., Japan’s second- largest bank by market value, led banks higher in Tokyo after the committee agreed to allow some deferred tax assets to be counted as capital. The nation’s banks and regulators had fought against excluding deferred tax assets.

“The Basel Committee’s easing of restrictions gives investors a reason to take another look at Japanese banks, which have been cheap recently,” said Mitsushige Akino, who oversees about $450 million in assets in Tokyo at Ichiyoshi Investment Management Co.

Sumitomo Mitsui rose 2.8 percent to 2,587 yen at the 3 p.m. close of trading in Tokyo. Mitsubishi UFJ Financial Group Inc., the country’s largest bank, gained 2.5 percent and Mizuho Financial Group Inc. climbed 2.2 percent.

‘Making Concessions’

“They’re definitely making concessions on the definition of capital and the liquidity ratios,” said BCM International’s Matthews, who used to lobby the committee on behalf of banks. “Those were necessary to convince the Germans to accept the leverage ratio. But even though we see a lot of concessions, there are also limits to the concessions. So this isn’t fully caving in.”

The Basel committee, which represents central banks and regulators in 27 nations and sets capital standards for banks worldwide, was asked by Group of 20 leaders to draft rules after the worst financial crisis in 70 years.

Yesterday’s agreements were announced after a meeting of the group of governors and heads of supervision, which oversees the committee’s work. While the committee narrowed differences when it met two weeks ago in Basel, it left most of the final decisions to its board, members said.

The board said some of its proposals might not be completed by the end of this year, the deadline set by the G-20. Liquidity requirements for how much cash and cashable securities banks need to hold against their longer-term liabilities and counter- cyclical buffers, which would raise minimum capital requirements in times of faster economic growth, have to be worked on longer, the board said.

Lobby Efforts

European banks lobbied against the proposed exclusion of minority interests that banks hold in other financial institutions. Japan fought the hardest against the elimination of deferred tax assets, past losses that lenders use to offset tax charges in future years. The U.S. has opposed removing mortgage-servicing rights, contracts to collect payments, which are unique to U.S. banks.

The compromise announced yesterday would allow a bank to count part of a stake it owns in another financial firm in relation to the risk the capital is supposed to cover at the entity in which it invested. Deferred tax assets and mortgage- servicing rights would be included in capital up to a limit. The total for all three could not exceed 15 percent of a lender’s common equity.

While the capital ratios allow banks to assign weights to assets based on their risks, the new leverage figure considers all assets without a risk assessment. The committee initially set it at 3 percent -- meaning a bank’s total assets cannot be more than 33 times its Tier 1 capital, which includes securities that could help a lender cover unexpected losses.

Level Playing Field

The new rule also defines how assets are tallied, so as to level the playing field between different accounting standards and bring off-balance-sheet items into the calculation. The ratio will be tested from 2013 until 2017, and banks would be required to start publishing their individual leverage figures starting in 2015.

Bankers including Deutsche Bank AG Chief Executive Officer Josef Ackermann and HSBC Holdings Plc Chairman Stephen Green have said that the new rules may force banks to reduce lending, potentially limiting economic growth.

While yesterday’s announcement resolved several issues, many areas of contention, such as the actual minimum capital ratios that will be set, remain outstanding, said KBW’s Cannon.

“The definition of capital had to be finalized before the numbers can be put on, but there are still many moving parts,” said Cannon, whose research firm specializes in financial companies. The committee is planning to present a final package of reforms to the G-20 leaders meeting in Seoul in November.

Risk-Weighted Assets

Banks currently need to hold capital equal to a minimum of 8 percent of risk-weighted assets. Half of that must be Tier 1, and half of the Tier 1 needs to be common stock. Both Tier 1 and common-equity ratios will be increased, Cannon and other analysts expect. The Basel committee is also revising how the risk weighting will be done.

Like the leverage ratio, the liquidity rules are new to the Basel standards. The liquidity coverage ratio sets the amount of cash that needs to be held by a lender against any payment coming due within a month, while the net stable funding ratio considers liabilities up to 12 months.

The committee announced several modifications to the definition of liquid assets and of how to measure the safety of different types of funding. Government deposits will now be considered the same as corporate cash put in a bank, instead of treated as other banks’ money as originally proposed. Bank deposits are seen as less stable.

The changes should please banks, said Cannon.

“They compromised more on the short-term ratio than we were expecting,” he said.

Sunday, September 29, 2013

"I am sure the euro will oblige us to introduce a new set of economic policy

instruments. It is politically impossible to propose that now. But some day

there will be a crisis and new instruments will be created."Romano Prodi, EU Commission President, 2001. The quote comes from a

interview Prodi had with Martin Wolf of the Financial Times which was published

on December 4th, 2001

"I am sure the euro will oblige us to introduce a new set of economic policy

instruments. It is politically impossible to propose that now. But some day

there will be a crisis and new instruments will be created."Romano Prodi, EU Commission President, 2001. The quote comes from a

interview Prodi had with Martin Wolf of the Financial Times which was published

on December 4th, 2001

Create a rainy day fund?

Look outside, its pouring down!

In a move that puts it on a collision course with Germany, the IMF discussion

note said that at a minimum, deeper fiscal integration required increased

policing of member states and the swift completion of a banking union with a

"common backstop" for eurozone lenders.

The report, titled: Toward a fiscal union for the euro area, said

forcing countries to endure repeated rounds of austerity to resolve future

crises would plunge weaker countries into a deflation spiral and drag the whole

region into a "prolonged period of stagnation."

It suggested that policymakers create a "rainy day fund", where governments

contributed up to €200bn (£168bn) a year to help weaker countries "ex-ante", and

avoid a systemic crisis.

The IMF economists also backed European Commission plans for a Single

Resolution Mechanism (SRM), which would hand a powerful central executioner the

power to wind down failing banks.

Germany has questioned the legality of the plans, which would hand sweeping

powers to Brussels, while none of the 28 EU member states have explicitly backed

them.

Monday, May 27, 2013

Hey Mario: what part of "FUCK OFF" don't you undestand.

EUROSMOKE AND LIES - “The answer to the crisis has not been less Europe but more Europe... The EU and

the [euro] are no exceptions. The choice is between adapting them to the new

conditions or do nothing and risk their dissolution.” The EU is a body

primarily driven by pure politics without any ameliorating rational input from

experts in economics markets science etc. Both the creation of the Eurozone and

the FTT were political projects making extensive use of confirmation bias and

totally ignoring expert advice. The Eurozone is a failure and the FTT will kill

off the City as well as destroy markets inside the EU which both sovereign

states and EU companies rely on. Politicians and bureaucrats taking the

decision have never even heard of the repo market but they are about to find out

how important it was once they destroy it. Rational thought would mean taking

account of the views of experts on the FTT but the FTT is a political dream

where there is no room for reality. If there was there would be no FTT. Any

organization run by purely political decisions is going to lose out against a

more rational response elsewhere in the world. I doubt the EU will ever base its

decisions on rational thought processes rather than politics as there is no

mechanism in place to force elite politicians to take note of experts. In their

conceit they only see their own narcissistic beliefs as relevant to decision

taking. Confirmation bias means that politicians start by already knowing the

answers and see the job as putting their irrational policies in place. When

policies do not work in the real world confirmation bias is called upon again to

warp data to explain failure without ever seeing any need to change policy.

Failure followed by more failure is guaranteed by the political approach.

Pressure from the UK public to leave will increase noticeably once the FTT is in

place and the City goes down the tubes. This will be extensively reported by the

media. How often have we heard this before? You will never convince the average

Brit that having more decisions taken by the unelected elite in Brussels is

going to deliver anything for us. The nearer you get to a EUSSR the less the

Brits will like it and the more we will want to leave. We have a totally

different mentality to the majority of the EU who think that taking all

decisions centrally will lead to economic success. That idea is seen as rubbish

here and unworldly. To work in the real world the people taking the decisions

would have to real experts in many fields and driven by rationality instead of

politics. That can never happen in the EU as it is a political construct.

Instead decisions are from over-conceited politicians and bureaucrats whose

knowledge and understanding of the real world is minimal. Whatever Draghi says

about banking reform will be politically based and not based on research by

experts. The starting point always has to be 'more EU' whereas it is unlikely in

the real world that all answers would come out to be simply as case of more EU

solving the problem. That is illogical. Draghi : "If we are successful in

establishing (a federal Europe) as I am sure we will be..." "Europe is much more

stable today (thanks to me)..." There you have it. Breathtaking arrogance

combined with delusion. The only option we have is to gtf away from pr!cks like

this.

Tuesday, March 26, 2013

The wounded, bleeding elephant in the room in Brussels today is the awful damage that has already been done to Europe's economy.

The wounded, bleeding elephant in the room in Brussels today is the awful damage that has already been done to Europe's economy.

Local firms in Cyprus saw business dried up as the country's banks remained closed, and customers learned the full scale of the crisis.

The looming capital controls (restrictions on cash withdrawals, bank transfers, etc) will hurt trade, possibly for months. And the destruction of parts of the Cypriot banking sector will take a great, big chunk out of the country's economy.

A well-respected fund manager based in London who blogs/tweets as Pawelmorski says the scale of the economic destruction achieved in the last week is unheard of 'without the use of weapons'.

He wrote yesterday....The combination of laying waste to the financial sector and tearing up the savings of thousands of residents means that Cyprus won’t return to current levels of output for a decade, a funeral pyre which bears comparison only with Greece. There are four shocks happening at once; the bog-standard austerity shock; the trauma of bank withdrawal controls; the wealth shock; and the structural shock of wiping out the financial sector. The bailout bill is certainly going to get a lot higher too, as a larger amount of debt is piled onto a smaller economy.

The central bank in Cyprus imposed a €100 a day withdrawal limit at cash machines for all local banks on Sunday to avert a run on lenders, as the island's leaders meet its international lenders for last-ditch talks to avert a financial meltdown.

The central bank in Cyprus imposed a €100 a day withdrawal limit at cash machines for all local banks on Sunday to avert a run on lenders, as the island's leaders meet its international lenders for last-ditch talks to avert a financial meltdown.

Sunday, March 24, 2013

Cyprus’s central bank said lenders would remain closed until at least Tuesday

amid growing speculation the Meditterranean island could become the eurozone

member to exit the currency bloc.

Cyprus’s central bank said lenders would remain closed until at least Tuesday

amid growing speculation the Meditterranean island could become the eurozone

member to exit the currency bloc.

Officials at the ECB were reported on Wednesday to be considering pulling the

plug on Cypriot banks unless the country agreed to a new bailout package.

Jörge Asmussen, the ECB’s chief negotiator, warned that Cyprus’s decision to

reject the terms of an €10bn (£8.6bn) bailout meant it could not guarantee

support to domestic lenders for much longer.

“We can provide emergency liquidity only to solvent banks and... the solvency

of Cypriot banks cannot be assumed if an aid programme is not agreed on soon,

which would allow for a quick recapitalisation of the banking sector,” said Mr

Asmussen in an interview with a German newspaper.

The threat followed the unanimous voting down by the Cypriot parliament

of a rescue package that would have seen the authorities levy a

“tax” of up to 10pc on deposits of more than €100,000.

Senior European politicians have expressed hope that a new bailout could be

organised, however some have begun to openly discuss the possibility of Cyprus

exiting the euro. Austrian Chancellor, Werner Faymann, said he could not “rule

anything out for Cyprus”.  German Chancellor Angela Merkel said she expected the Cypriot government to

come up with a new rescue plan, but continued to insist it was fair for large

depositors in Cypriot banks to face a loss on their savings.

German Chancellor Angela Merkel said she expected the Cypriot government to

come up with a new rescue plan, but continued to insist it was fair for large

depositors in Cypriot banks to face a loss on their savings.

Banks in Cyprus have remained closed since last week and on Wednesday the

country’s central bank said lenders would not open their doors until next

Tuesday, leaving Cypriots dependent on using ATMs for day-to-day cash. The prolonged closure of banks has led to widespread fears among senior

industry executives that it could undermine confidence in the financial system.

Christian Clausen, president of the European Banking Federation, said a way

had to be found to reopen Cypriot banks before it was “too late”.

“Everything needs to be solved very quickly. This is a matter of a very few

days before it gets too late,” Mr Clausen told Reuters... While the eurozone finance ministers are busy having their conference call,

Bloomberg reports that the currency bloc's finance chiefs are pressuring Cyprus

to shrink its banking system. Here's what the newswire had to

say:

Finance ministers for the 17 euro countries are considering a plan to

shutter the two biggest banks in Cyprus and freeze the assets of uninsured

depositors, said the four officials, who asked not to be named because the talks

are ongoing. The ministers are holding a teleconference tonight.

Finance ministers for the 17 euro countries are considering a plan to

shutter the two biggest banks in Cyprus and freeze the assets of uninsured

depositors, said the four officials, who asked not to be named because the talks

are ongoing. The ministers are holding a teleconference tonight.

UPDATE : Cyprus Popular Bank and the Bank of Cyprus would be split to create a so-called bad bank, one of the officials said.

Insured deposits -- below the European Union ceiling of 100,000 euros -- would go into a so-called good bank and not sustain any losses, while uninsured deposits would go into the bad bank and be frozen until assets could be sold, said the four officials.

Finance ministers for the 17 euro countries are considering a plan to

shutter the two biggest banks in Cyprus and freeze the assets of uninsured

depositors, said the four officials, who asked not to be named because the talks

are ongoing. The ministers are holding a teleconference tonight.

Finance ministers for the 17 euro countries are considering a plan to

shutter the two biggest banks in Cyprus and freeze the assets of uninsured

depositors, said the four officials, who asked not to be named because the talks

are ongoing. The ministers are holding a teleconference tonight. UPDATE : Cyprus Popular Bank and the Bank of Cyprus would be split to create a so-called bad bank, one of the officials said.

Insured deposits -- below the European Union ceiling of 100,000 euros -- would go into a so-called good bank and not sustain any losses, while uninsured deposits would go into the bad bank and be frozen until assets could be sold, said the four officials.

Losses to unsecured creditors, including uninsured depositors, could reach

40 percent under the plan, which has support from the International Monetary

Fund and the European Central Bank. hile the eurozone finance ministers are busy having their conference call,

Bloomberg reports that the currency bloc's finance chiefs are pressuring Cyprus

to shrink its banking system. Here's what the newswire had to

say:

Finance ministers for the 17 euro countries are considering a plan to

shutter the two biggest banks in Cyprus and freeze the assets of uninsured

depositors, said the four officials, who asked not to be named because the talks

are ongoing.

Russians in Cyprus are getting tired of suggestions from Germany that anyone with a Russian accent here is a Mafioso. They say that claims that the island is simply a money-laundering post for Mob cash are wide of the mark, and that the EU strategy has been purely a political one.

"Since this started happening the German, Dutch, and Scandinavian treasuries have been doing very well while the quotes for southern European ones have gone down," says Andrei Surikov, 30, a financial manager from Moscow who moved to Cyprus three years ago.

"The whole thing is just a dirty political game, and I don't think the EU has estimated the impact of what they have done. The trust has gone now in the whole system."

Russians in Cyprus are getting tired of suggestions from Germany that anyone with a Russian accent here is a Mafioso. They say that claims that the island is simply a money-laundering post for Mob cash are wide of the mark, and that the EU strategy has been purely a political one.

"Since this started happening the German, Dutch, and Scandinavian treasuries have been doing very well while the quotes for southern European ones have gone down," says Andrei Surikov, 30, a financial manager from Moscow who moved to Cyprus three years ago.

"The whole thing is just a dirty political game, and I don't think the EU has estimated the impact of what they have done. The trust has gone now in the whole system."

Saturday, January 5, 2013

French President François Hollande pledged to reverse the country’s surging unemployment rate as he gave his first New Year’s televised address at the Elysée Palace on Monday.

French President François Hollande pledged to reverse the country’s surging unemployment rate as he gave his first New Year’s televised address at the Elysée Palace on Monday.

Speaking of the “serious and legitimate” concerns of the public, Hollande acknowledged the “fits and starts” of his first six months in office, but said France would emerge from the financial crisis “sooner and stronger” than expected because of the course he and his government had taken. “We’ve set the course – jobs, competitiveness and growth – and I will not deviate. It’s the future of France.”

With the number of jobless breaking the three-million barrier for the first time this year, Hollande said “all our efforts will be aimed at a single objective: reversing the unemployment trend within a year, whatever the cost”.

He also promised to tackle what he described as “useless spending” in government. “The French public’s money is hard earned and must be put to the service of a thrifty and exemplary state”.

“Those with more will have to contribute more”

But speaking of his controversial 75% income tax levy, which was overturned by France’s highest legal body on Saturday, the Socialist president said that while the law would be “redesigned” its objective would remain the same. “Those with more will have to contribute more,” he said.

Hollande also stressed the increase in teacher numbers he promised during his election manifesto and touted his delivery of promises to allow 60-year-olds the right to retire if they began working early, along with the return of French combat troops from Afghanistan.

Briefly mentioning the controversial issues of same-sex marriage and euthanasia, Hollande stressed the importance of civil rights. “We have all it takes to succeed,” he said, adding that France is most successful “when it moves forward on equal rights”.

Ending his address with a thought for the “sick, lonely, disabled and unassisted” people in France, the French president said social security was as important as a competitive economy and called for a “collective effort” to make that balance possible.

Monday, December 24, 2012

EU leaders have agreed on a roadmap

for eurozone integration beyond the deal on centralised banking supervision,

German Chancellor Angela Merkel said.

Specific dates have not yet been agreed for the phases of integration. But the EU summit chairman, Herman Van Rompuy, said a deal should be reached

next year on a joint resolution scheme for winding up failed banks.

Specific dates have not yet been agreed for the phases of integration. But the EU summit chairman, Herman Van Rompuy, said a deal should be reached

next year on a joint resolution scheme for winding up failed banks.

Mr Van Rompuy's far-reaching

roadmap was the main topic of the two-day Brussels summit. Speaking after the summit talks, French President Francois Hollande said:

"There is no doubt today about the integrity of the eurozone - Europe cannot now

be taken by surprise."

But beyond the banking reforms, he said, Europe must address the problems of

unemployment and feeble growth.

The deal to make the European Central Bank (ECB) the chief regulator should

pave the way for direct recapitalisation of struggling eurozone banks by the

main bailout fund, the 500bn-euro (£406bn; $654bn) European Stability Mechanism

(ESM). Spain is especially anxious to get that help for its debt-laden banks.

Direct recapitalisation would help break the "vicious circle" in which bank

debts have put a crippling burden on national budgets and led to massive

taxpayer-funded bailouts. However, Germany insists that the ESM should not be used to write off the

existing "legacy" debts that have burdened Spain, Greece and the Republic of

Ireland. Any ESM loans will be accompanied by tough rules on budget discipline.

Friday, December 21, 2012

Italian Prime Minister Mario Monti resigned on Friday after a year of battling

the debt crisis with austerity and reforms and selling his nation to the

germans as lawmakers gave final approval to a budget bill that will pave the way

for early elections. Monti said earlier he would step down once the vote was

approved, kicking off a campaign that will likely see Italy go to the polls on

February 24, with former premier Silvio Berlusconi and centre-left leader Pier

Luigi Bersani already in the running. After Christmas mass in the prime

minister's residence, Monti joked about the end-of-world Mayan prophecy saying:

"A year ago this government was only just beginning. Now we will have to wrap up

and it's not the fault of the Mayas." He then addressed Italy's ambassadors

abroad saying his speech would be his "last act" before handing in his

resignation. "Thank you for these difficult but fascinating 13 months," he

said. Monti could also join the campaign and is under strong domestic and

international pressure to do so. He is expected to reveal his future political

ambitions at an end of year press conference scheduled for Sunday. Sources

close to the technocrat premier insist he has not yet decided whether to enter

the fray, despite appearing to launch a bid for a weighty role in the campaign

with a rousing speech at a Fiat factory on Thursday. Some political observers

have said Monti could campaign as unofficial leader of a centrist coalition that

has been likened to the Christian-Democrats who dominated Italy for decades.

Monti's name cannot officially be on the ballot as he is already a senator for

life, but he can still be appointed to a post in government including prime

minister or finance minister after elections. The centrist agenda will include

"historic reforms" and "far deeper liberalization than we have witnessed so

far", sources quoted by the Corriere della Sera daily. Monti, 69, defended on

Thursday the "bitter medicine" of budget discipline he has implemented as well

as his selling his people to the "Fourth Reich" and warned against any attempt

to turn back the clock. Another words, he wants a German governor and a nation

of enslaved Italians!!!

Italian Prime Minister Mario Monti resigned on Friday after a year of battling

the debt crisis with austerity and reforms and selling his nation to the

germans as lawmakers gave final approval to a budget bill that will pave the way

for early elections. Monti said earlier he would step down once the vote was

approved, kicking off a campaign that will likely see Italy go to the polls on

February 24, with former premier Silvio Berlusconi and centre-left leader Pier

Luigi Bersani already in the running. After Christmas mass in the prime

minister's residence, Monti joked about the end-of-world Mayan prophecy saying:

"A year ago this government was only just beginning. Now we will have to wrap up

and it's not the fault of the Mayas." He then addressed Italy's ambassadors

abroad saying his speech would be his "last act" before handing in his

resignation. "Thank you for these difficult but fascinating 13 months," he

said. Monti could also join the campaign and is under strong domestic and

international pressure to do so. He is expected to reveal his future political

ambitions at an end of year press conference scheduled for Sunday. Sources

close to the technocrat premier insist he has not yet decided whether to enter

the fray, despite appearing to launch a bid for a weighty role in the campaign

with a rousing speech at a Fiat factory on Thursday. Some political observers

have said Monti could campaign as unofficial leader of a centrist coalition that

has been likened to the Christian-Democrats who dominated Italy for decades.

Monti's name cannot officially be on the ballot as he is already a senator for

life, but he can still be appointed to a post in government including prime

minister or finance minister after elections. The centrist agenda will include

"historic reforms" and "far deeper liberalization than we have witnessed so

far", sources quoted by the Corriere della Sera daily. Monti, 69, defended on

Thursday the "bitter medicine" of budget discipline he has implemented as well

as his selling his people to the "Fourth Reich" and warned against any attempt

to turn back the clock. Another words, he wants a German governor and a nation

of enslaved Italians!!!Friday, December 14, 2012

A political and economic system in which underachievers forcibly redistribute their mediocrity to the rest of society

Life is actually much better for European working class than in the US. US

workers are more and more like obedient little slaves, working two jobs just to

earn enough for living. 10-12 hour days and maybe two weeks holiday per year.

Then they eat shit food which basically poisons them over the decades slowly but

surely, causing high cholesterol, hypertension, diabetes and all sorts of other

sicknesses. When they got sick, their health insurance is a form of financial

torture, designed to find ways to not to pay. Public education is quite crappy

and social safety nets are mostly missing.

The creation of the EU and the common currency was never anything more than a

thinly veiled campaign to force European nations into a monolithic Socialist

union and help the new Soviet Union (EEC) acquire the production and energetic

capacities of Europe, while Germany gets to "administer" the EU states.

Economists around the globe warned of the consequences and kept on warning over

the last 15 -20 years. The voters in Europe ignored the harsh facts and instead

chose bread and circus... and now they reap the benefits of their stupidity and

greed. The Forth Reich is ruling Europe since the "independent union nations"

budgets have to be approved by the Bundestag before being implemented !!!

Deucland uber ales !!!

In a dramatic about-turn, German Finance Minister Wolfgang Schaeuble ditched

his earlier objections that had led him to clash openly with his French

counterpart, Pierre Moscovici, last week over the ECB's role in banking

supervision.

In a dramatic about-turn, German Finance Minister Wolfgang Schaeuble ditched

his earlier objections that had led him to clash openly with his French

counterpart, Pierre Moscovici, last week over the ECB's role in banking

supervision.

With time running out to meet a year-end deadline, both sides managed to settle their differences and Germany won concessions to temper the authority of the ECB's Governing Council over the new supervisor.

Agreement on bank surveillance is a crucial first step towards a broader "banking union," or common euro zone approach to dealing with failing banks that in recent years dragged down countries such as Ireland and Spain.

The next pillar of a banking union would be the creation of a central system to close troubled banks.

The decision also sends a strong signal to investors that the euro zone's 17 members, from powerful Germany to stricken Greece, can pull together to tackle the bloc's problems.

In a dramatic about-turn, German Finance Minister Wolfgang Schaeuble ditched

his earlier objections that had led him to clash openly with his French

counterpart, Pierre Moscovici, last week over the ECB's role in banking

supervision.

In a dramatic about-turn, German Finance Minister Wolfgang Schaeuble ditched

his earlier objections that had led him to clash openly with his French

counterpart, Pierre Moscovici, last week over the ECB's role in banking

supervision. With time running out to meet a year-end deadline, both sides managed to settle their differences and Germany won concessions to temper the authority of the ECB's Governing Council over the new supervisor.

Agreement on bank surveillance is a crucial first step towards a broader "banking union," or common euro zone approach to dealing with failing banks that in recent years dragged down countries such as Ireland and Spain.

The next pillar of a banking union would be the creation of a central system to close troubled banks.

The decision also sends a strong signal to investors that the euro zone's 17 members, from powerful Germany to stricken Greece, can pull together to tackle the bloc's problems.

Tuesday, December 4, 2012

Tying disparate countries to one exchange rate simply makes no sense

When will the polititians realize that tying disparate countries to one exchange

rate simply makes no sense?... How can Greece share a currency and monetary

framework with Germany? A totally idiotic concept. The Euro is the PROBLEM

!!! A single currency cannot provide a solution. The eurozone was dealt a

fresh blow as Moody’s Investors Service downgraded the region’s rescue funds and

unemployment hit a new record high. The ratings agency cut its rating on the

European Stability Mechanism to AA1 from AAA and maintained a negative outlook.

It also lowered the European Financial Stability Facility’s provisional rating

to (P)AA1 from (P)AAA. Moody’s said its decision was driven by its recent

downgrade of France, because the credit risk and ratings of the rescue funds

were “closely aligned to those of its strongest supporters” ...Klaus Regling,

managing director of the ESM and chief executive of EFSF, said Moody’s decision

was “difficult to understand.” He added: “We disagree with the rating agency’s

approach which does not sufficiently acknowledge ESM’s exceptionally strong

institutional framework, political commitment and capital structure.” It came

as the EU’s statistics office said eurozone unemployment rose to 11.7pc in

October from 11.6pc in September.... Have idiotic and arrogant politicians

worldwide not realised that ideological half ars.ed constructions like the EU

and the EZ always fail ? Are we really surprised that it was Europe with its

history of fascism, communism, military dictatorship and undemocratic statist

and authoritarian governments which has given birth to two of the most appalling

and undemocratic constructions of the 20th century, the EU and the EZ ? They

will fail just like the USSR failed. "Klaus Regling, managing director of the

ESM and chief executive of EFSF said: Moody’s decision was “difficult to

understand.” They should get someone with more understanding. I wonder what he

gets paid for having so little of the stuff? 150,000€ a year?.... Well, I must

write to the EU and tell them that my 90 year-old Gran is currently available.

She used to run a market stall and so understands economics. Sadly, she is now

showing signs of senile dementia, but even so, it must be worth a go compared to

the current lot.

When will the polititians realize that tying disparate countries to one exchange

rate simply makes no sense?... How can Greece share a currency and monetary

framework with Germany? A totally idiotic concept. The Euro is the PROBLEM

!!! A single currency cannot provide a solution. The eurozone was dealt a

fresh blow as Moody’s Investors Service downgraded the region’s rescue funds and

unemployment hit a new record high. The ratings agency cut its rating on the

European Stability Mechanism to AA1 from AAA and maintained a negative outlook.

It also lowered the European Financial Stability Facility’s provisional rating

to (P)AA1 from (P)AAA. Moody’s said its decision was driven by its recent

downgrade of France, because the credit risk and ratings of the rescue funds

were “closely aligned to those of its strongest supporters” ...Klaus Regling,

managing director of the ESM and chief executive of EFSF, said Moody’s decision

was “difficult to understand.” He added: “We disagree with the rating agency’s

approach which does not sufficiently acknowledge ESM’s exceptionally strong

institutional framework, political commitment and capital structure.” It came

as the EU’s statistics office said eurozone unemployment rose to 11.7pc in

October from 11.6pc in September.... Have idiotic and arrogant politicians

worldwide not realised that ideological half ars.ed constructions like the EU

and the EZ always fail ? Are we really surprised that it was Europe with its

history of fascism, communism, military dictatorship and undemocratic statist

and authoritarian governments which has given birth to two of the most appalling

and undemocratic constructions of the 20th century, the EU and the EZ ? They

will fail just like the USSR failed. "Klaus Regling, managing director of the

ESM and chief executive of EFSF said: Moody’s decision was “difficult to

understand.” They should get someone with more understanding. I wonder what he

gets paid for having so little of the stuff? 150,000€ a year?.... Well, I must

write to the EU and tell them that my 90 year-old Gran is currently available.

She used to run a market stall and so understands economics. Sadly, she is now

showing signs of senile dementia, but even so, it must be worth a go compared to

the current lot.Tuesday, November 6, 2012

WSJ - about the election day ...

WSJ - We begin with the three words everyone writing about the election must say:

Nobody knows anything. Everyone’s guessing. I spent Sunday morning in Washington

with journalists and political hands, one of whom said she feels it’s Obama, the

rest of whom said they don’t know. I think it’s Romney. I think he’s stealing in

“like a thief with good tools,” in Walker Percy’s old words. While everyone is

looking at the polls and the storm, Romney’s slipping into the presidency. He’s

quietly rising, and he’s been rising for a while.

WSJ - We begin with the three words everyone writing about the election must say:

Nobody knows anything. Everyone’s guessing. I spent Sunday morning in Washington

with journalists and political hands, one of whom said she feels it’s Obama, the

rest of whom said they don’t know. I think it’s Romney. I think he’s stealing in

“like a thief with good tools,” in Walker Percy’s old words. While everyone is

looking at the polls and the storm, Romney’s slipping into the presidency. He’s

quietly rising, and he’s been rising for a while.

Obama and the storm, it was like a wave that lifted him and then moved on,

leaving him where he’d been. Parts of Jersey and New York are a cold Katrina.

The exact dimensions of the disaster will become clearer when the election is

over. One word: infrastructure. Officials knew the storm was coming and everyone

knew it would be bad, but the people of the tristate area were not aware, until

now, just how vulnerable to deep damage their physical system was. The people in

charge of that system are the politicians. Mayor Bloomberg wanted to have the

Marathon, to show New York’s spirit. In Staten Island last week they were

bitterly calling it “the race through the ruins.” There is a disconnect.

But to the election. Who knows what to make of the weighting of the polls and

the assumptions as to who will vote? Who knows the depth and breadth of each

party’s turnout efforts? Among the wisest words spoken this cycle were by John

Dickerson of CBS News and Slate, who said, in a conversation the night before

the last presidential debate, that he thought maybe the American people were

quietly cooking something up, something we don’t know about.

I think they are and I think it’s this: a Romney win.

Romney’s crowds are building—28,000 in Morrisville, Pa., last night; 30,000

in West Chester, Ohio, Friday It isn’t only a triumph of advance planning:

People came, they got through security and waited for hours in the cold.

His rallies look like rallies now, not enactments. In some new way he’s caught

his stride. He looks happy and grateful. His closing speech has been positive,

future-looking, sweetly patriotic. His closing ads are sharp—the one about

what’s going on at the rallies is moving.

All the vibrations are right. A person who is helping him who is not a

longtime Romneyite told me, yesterday: “I joined because I was anti Obama—I’m a

patriot, I’ll join up But now I am pro-Romney.” Why? “I’ve spent time with him

and I care about him and admire him. He’s a genuinely good man.” Looking at the

crowds on TV, hearing them chant “Three more days” and “Two more days”—it feels

like a lot of Republicans have gone from anti-Obama to pro-Romney.

Sunday, November 4, 2012

What's worse than an unelected hack steamrolling the lives of ordinary people?

Ireland's former attorney general, former minister for Justice and now

practicing senior council one Michael McDowell was on national radio earlier

today, wondering out loud why the country was not debating a Federal Europe that

is being foisted on small countries by dint of an economic crisis exported from

the core to the periphery. He wondered why Ireland was not paying enough attention to the UK's efforts

to de-couple itself from core competencies and obligations being foisted on it

by EU "Euro fascists" (my words). He wondered, if crossing the border from the

Irish republic was going to be akin to crossing the border from East Germany

into West Berlin during the dark days of the USSR. Entering the land of the

free?I agree with his sentiments, federalism is a complete misnomer, buried deep

inside the velvet glove of federalism is the Iron fist that will be used more

and more boldly to smash the sovereign nation state. It is nothing less than a

takeover of most states within Europe by Wolfgang, Von Rompuy and other

egotistical men such as Barroso and Rehn. Dangerous people who know not what

they are unleashing across the Eruopean continent. These are people who would

barely get people to cross the road with them under their banner of a federalist

Europe but who are marveling at the power an economic crisis has bestowed upon

them. Small wonder they want to make crisis permanent? It is the UK once again

who are standing up for what is left of democracy in Europe and god knows that

in itself tells us a lot about how far the rot has gone because we know that

democracy in Britain itself has been significantly eroded over the last 40

years.

Ireland's former attorney general, former minister for Justice and now

practicing senior council one Michael McDowell was on national radio earlier

today, wondering out loud why the country was not debating a Federal Europe that

is being foisted on small countries by dint of an economic crisis exported from

the core to the periphery. He wondered why Ireland was not paying enough attention to the UK's efforts

to de-couple itself from core competencies and obligations being foisted on it

by EU "Euro fascists" (my words). He wondered, if crossing the border from the

Irish republic was going to be akin to crossing the border from East Germany

into West Berlin during the dark days of the USSR. Entering the land of the

free?I agree with his sentiments, federalism is a complete misnomer, buried deep

inside the velvet glove of federalism is the Iron fist that will be used more

and more boldly to smash the sovereign nation state. It is nothing less than a

takeover of most states within Europe by Wolfgang, Von Rompuy and other

egotistical men such as Barroso and Rehn. Dangerous people who know not what

they are unleashing across the Eruopean continent. These are people who would

barely get people to cross the road with them under their banner of a federalist

Europe but who are marveling at the power an economic crisis has bestowed upon

them. Small wonder they want to make crisis permanent? It is the UK once again

who are standing up for what is left of democracy in Europe and god knows that

in itself tells us a lot about how far the rot has gone because we know that

democracy in Britain itself has been significantly eroded over the last 40

years.

Saturday, November 3, 2012

Comments on EURO-JOBLESS rise: I believe that the politicians have let us down, are continuing to do so and will carry on doing it. Where I digress is that I believe they do not tell us the whole truth. And here i am thinking about Balls and Milliband junior who try to seduce us with easy solutions when there are none. This is a long haul and we have to cut Govt spending. to say otherwise is either cloud cuckoo land or lies.Although the unemployment figures are still dreadful I am assuming that the slight reduction in Portugal’s rates would have to do with seasonal work related to tourism which always influences partial figures for Q2 and Q3. Probably not really a trend, unfortunately.

Comments on EURO-JOBLESS rise: I believe that the politicians have let us down, are continuing to do so and will carry on doing it. Where I digress is that I believe they do not tell us the whole truth. And here i am thinking about Balls and Milliband junior who try to seduce us with easy solutions when there are none. This is a long haul and we have to cut Govt spending. to say otherwise is either cloud cuckoo land or lies.Although the unemployment figures are still dreadful I am assuming that the slight reduction in Portugal’s rates would have to do with seasonal work related to tourism which always influences partial figures for Q2 and Q3. Probably not really a trend, unfortunately.

And I wonder, as with Greece, if reality isn’t a bit worse in Portugal as I read a lot of reports of companies that don’t pay their employees. So, they are neither unemployed nor in meaningful employment. A bookshop chain where I regularly buy most of my literature apparently only pays their employees one wage every 3 months. Portuguese law only allows for a contract to be cancelled by an employee with a justifiable reason for non-payments if these are not paid for 3 months. In this case this means that the employees cannot have access to the Portuguese equivalent of JSA or ESA but can’t also cancel their contract with justifiable reason, which would allow them to eventually claim those benefits. If they were to cancel their contracts at this stage they would actually need to pay probably pay some money back to the company as severance but would also lose all rights to claim for their missed wages for previous months....There is an alternative. A very good one. Watch. A bank charges interest to a firm which means it earns interest and can pay its staff. The staff then spend their money at the firm and get stuff the firm produces for them. The firm now has the income which it can use to pay the bank interest. Monetary result is zero (the bank interest charged paid for itself), but real goods and services were produced and transferred to bank staff. Money and goods are not the same thing. They operate in different circuits and respond in different ways. Why have a bank issuing money out of thin air?, that is still a Monetary based system. Why not have a Resource based system?. An economy based upon meeting peoples needs (and desires) while accepting there are finite resources in the world to be shared amongst the population. Any system based upon interest is fundamentally flawed and damages us and the environment in the long run.

Wednesday, October 24, 2012

The fourth REICH in full action according to the Ribbentrop - Molotov Treaty ... Europe is under the German boot !!!!..

Mario Draghi has defended his Outright Monetary Transactions plan to the Bundestag in the last few minutes.

Draghi promised German MPs that the pledge to buy unlimited quantities of bonds will dispel fears over the euro's future.

The ECB president also began his two-hour appearance in Berlin by repeating his line that politicians, not central bankers, must take the decisive steps to ensure Europe's future

The ECB president also began his two-hour appearance in Berlin by repeating his line that politicians, not central bankers, must take the decisive steps to ensure Europe's future

Here's how Draghi defended the OMT, which he insisted did not put taxpayers at risk.

We designed the OMTs exactly to...restore monetary policy transmission in two key ways.First, it provides for ex ante unlimited interventions in government bond markets, focusing on bonds with a remaining maturity of up to three years. A lot of comments have been made about this commitment. But we have to understand how markets work. Interventions are designed to send a clear signal to investors that their fears about the euro area are baseless.Second, as a pre-requisite for OMTs, countries must have negotiated with the other euro area governments a European Stability Mechanism (ESM) programme with strict and effective conditionality. This ensures that governments continue to correct economic weaknesses while the ECB is active. The involvement of the IMF, with its unparalleled track record in monitoring adjustment programmes would be an additional safeguard.

Draghi also warned that deflation is a bigger risk than inflation today, which may not convince German lawmakers who fear a return to the 1920s.

Saturday, October 20, 2012

European leaders early Friday agreed to have a new supervisor for euro-zone banks up and running next year, a step that will pave the way for the bloc's bailout fund to pump capital directly into banks throughout the single-currency area......

Friday's announcement is a disappointment for some officials at the European Commission, the EU's executive arm, who had hoped to have the supervisor operational at the start of 2013.

The leaders also discussed plans for a common budget for the 17 euro-zone nations that could be used to absorb economic shocks impacting one part of the euro zone but not others. But José Manuel Barroso, the commission president, said: "This is something for the medium and longer term.

The man who died in Greece :

The death came as protesters lobbed flares, petrol bombs and chunks of marble at lines of riot police, who responded with tear gas and stun grenades, in confrontations which have become all too familiar in the Greek capital over the last three years.

Friday's announcement is a disappointment for some officials at the European Commission, the EU's executive arm, who had hoped to have the supervisor operational at the start of 2013.

The leaders also discussed plans for a common budget for the 17 euro-zone nations that could be used to absorb economic shocks impacting one part of the euro zone but not others. But José Manuel Barroso, the commission president, said: "This is something for the medium and longer term.

The man who died in Greece :

The death came as protesters lobbed flares, petrol bombs and chunks of marble at lines of riot police, who responded with tear gas and stun grenades, in confrontations which have become all too familiar in the Greek capital over the last three years.

The clashes erupted in and around Syntagma Square, in front of parliament,

during protests against a new wave of austerity cuts that the government plans

to introduce in November.

"A 65-year-old man was taken to hospital where efforts to revive him

failed," a health ministry official told the AFP news agency.

One report said the man had been found dead in Syntagma Square while

another said he was found on a bench several hundred yards from the violence.

Friday, October 12, 2012

A pathetic gesture by a group of Nordic Europhiles intended to boost EU morale in dark times.

Has the committee which runs the Nobel Peace Prize been infiltrated by satirists or opponents keen on discrediting the organisation? Norwegian radio reports this morning, carried by Reuters, suggested that the European Union is to be awarded the prize for supposedly keeping the peace in Europe for the last sixty years. Was this a Nordic spoof? Apparently not.

Has the committee which runs the Nobel Peace Prize been infiltrated by satirists or opponents keen on discrediting the organisation? Norwegian radio reports this morning, carried by Reuters, suggested that the European Union is to be awarded the prize for supposedly keeping the peace in Europe for the last sixty years. Was this a Nordic spoof? Apparently not.

It is only a few years since President Obama was ludicrously awarded the Nobel peace prize for winning the 2008 election and not being George Bush. Since then Mr Obama has continued the war in Afghanistan, stepped up drone attacks and got America involved in Libya's bloody revolution, suggesting that it is better to hand out baubles after someone has finished their job rather than when they are just getting started or are half way through. Incidentally, the same stricture should have applied to bankers honoured by New Labour when they were still running banks which later blew up.

Giving the EU a peace prize is at best premature, like knighting Sir Fred Goodwin in the middle of the mad boom. We have no idea how the experiment to create an anti-democratic federation will end. Hopefully the answer is very peacefully, but when Greek protesters are wearing Nazi uniforms, and Spanish youth unemployment is running at 50 per cent, a look at history suggests there is always the possibility of a bumpy landing.

Daftest of all is the notion that the EU itself has kept the peace. It was the Allies led by the Americans, the Russians and the British who defeated and disarmed the Germans in 1945. The German people then underwent the most extraordinary reckoning, transforming their country into an essentially pacifist society. The EU had very little to do with it. Throughout that period it was Nato, led by the Americans and British, which kept the peace in Western Europe. The American taxpayer picked up most of the resulting tab, and the British paid a significant part of the bill too.

Under this defence umbrella, the federalists who wanted to reconstruct the notion of Carolingian Empire which dominated 9th century Europe, created what we have come to know and love as the EU. Of course there are advantages in what they constructed – the single market and easier travel, making the South of France and Tuscany more accessible. But they also built an appallingly designed single currency, a horlicks of an agricultural policy and rapacious bureaucracy determined to stifle the nation state in the name of utopian, unachievable continent-wide homogeneity. And at every turn those driving it looked for ways to outwit the democratic will.

It is said that those in charge of the Nobel Peace Prize have made their latest award to distract attention from the eurozone crisis, which only adds a further surreal twist. The last year or so in Europe has been marked by demonstrations and extensive European rioting. There are words one can use to describe what is going on, but "peaceful" isn't one of them.(By Iain Martin

Subscribe to:

Posts (Atom)