The US government was forced to begin closing swathes of non-essential services on Tuesday morning after frantic rounds of late night political sparring failed to avert the first federal shutdown in nearly two decades.

As a midnight deadline to extend Congressional spending authority ticked ever closer, Republicans staged a series of last-ditch efforts to use a once-routine budget procedure to force Democrats to abandon their efforts to extend US health insurance.

Three separate attacks on the Affordable Care Act, known as Obamacare, were staged by the House of Representatives, only to be rejected in turn by the Democrat-controlled Senate, which accused Republicans of holding the country to ransom.

Shortly before midnight, Senate majority leader Harry Reid marked the end of the process by rejecting House calls for formal talks to reconcile their conflicting positions, arguing it was impossible to negotiate with a “gun to our heads”.

“This is a very serious time in the history of our country,” Reid said. “Millions of people are going to be affected tomorrow and the Republicans are still playing games”

An estimated 800,000 federal workers will be forced to stay at home from Tuesday under a stalemate that could drag on for days and disrupt services as varied as national parks and the US space programme.

The White House has drawn up a list of essential staff who are legally allowed to carry on working, but President Barack Obama warned that a shutdown would have an immediate affect on the fragile US economy.

“We do not have a clear indication that Congress will act in time for the president to sign a Continuing Resolution before the end of the day tomorrow, October 1,” said a White House statement issued shortly before midnight.

“Therefore, agencies should now execute plans for an orderly shutdown due to the absence of appropriations. We urge Congress to act quickly to pass a Continuing Resolution to provide a short-term bridge that ensures sufficient time to pass a budget for the remainder of the fiscal year, and to restore the operation of critical public services and programs that will be impacted by a lapse in appropriations.”

Obama also issued a statement to military employees after signing a Republican-proposed law that exempts active-duty servicemen from the effects of the shutdown, but will not protect civilian workers.

“I know the days ahead could mean more uncertainty, including possible furloughs,” Obama said. “You and your families deserve better than the dysfunction we’re seeing in Congress.”

House speaker John Boehner denied that Republican tactics were responsible for the shutdown, insisting Democrats were to blame for refusing to negotiate over Obamacare.

“I didn't come here to shut down the government,” Boehner told one of several heated House debates.

“I came here to fight for a smaller, less costly and more accountable federal government. But here we find ourselves in this moment dealing with a law that’s causing unknown consequences and unknown damage to the American people and to our economy. And that issue is Obamacare.”

But Democrats are confident that US public opinion will continue to hold Republicans to blame for what could be days of disruption until a deal can be struck.

They argue that Republicans are using underhand methods to overturn a law that was passed four years ago, ratified by the supreme court and endorsed by voters at the last presidential election.

Senator Bernie Sanders, of Vermont, said: “If we surrender to hostage-taking tonight, these guys would be back within a couple of weeks without a shadow of a doubt. What we are dealing with tonight is an extraordinary anti-democratic act.”

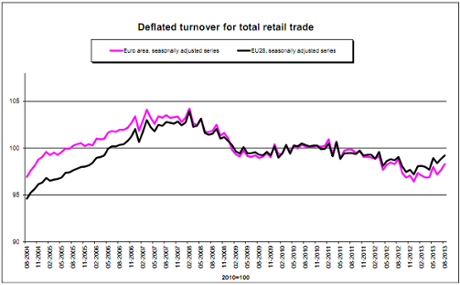

Good news for the European economy: retail sales were much stronger than expected in August.

Good news for the European economy: retail sales were much stronger than expected in August.

Cyprus will no be the model for future EU bailouts

Cyprus will n be the model for future EU bailouts

Cyprus will be the model for future EU bailouts.

EU word games.

Just like all Humpty Dumpty outfits - when they use a word it means whatever they want it to mean.